Circle Internet GroupNYSE:CRCL

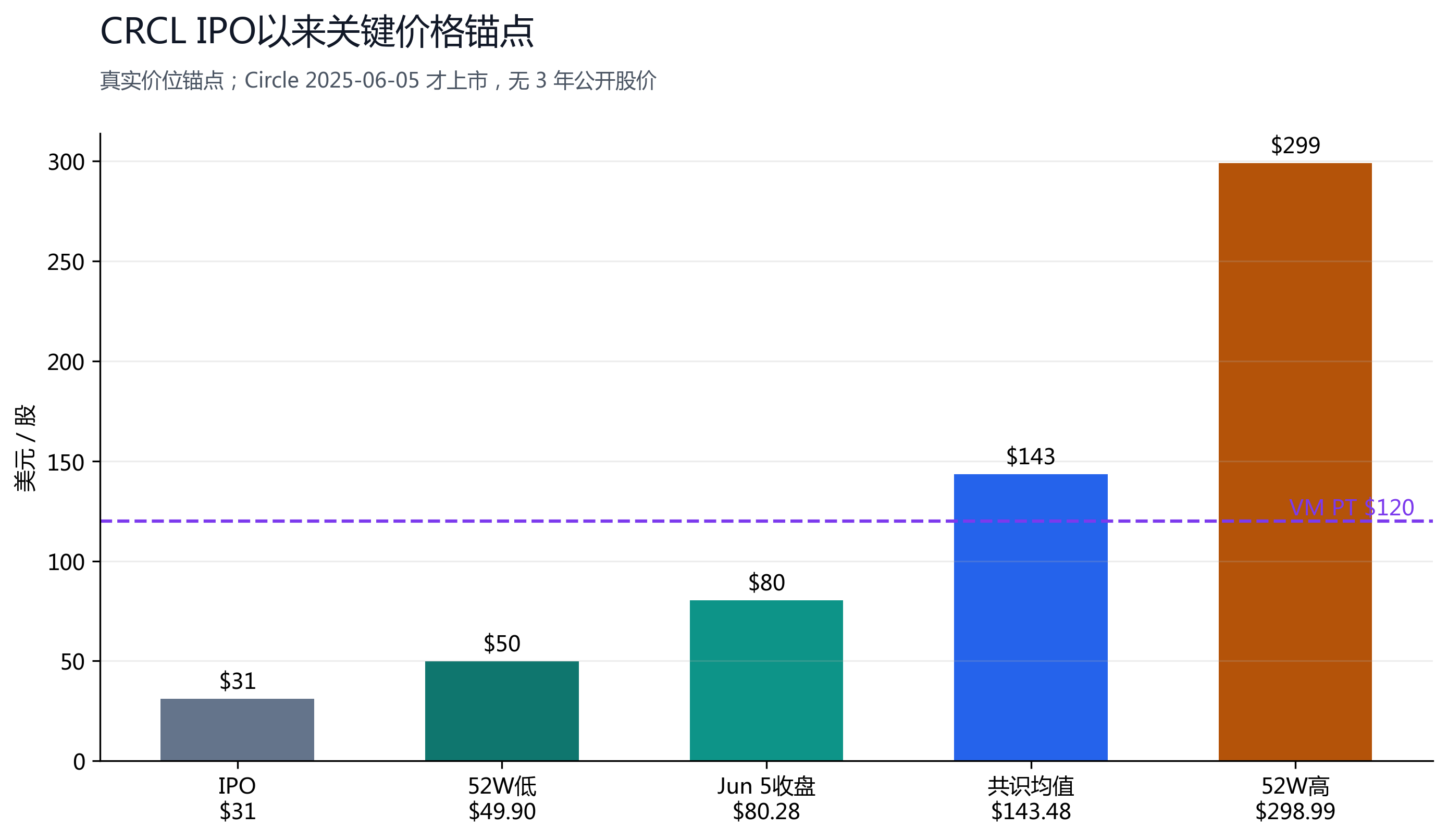

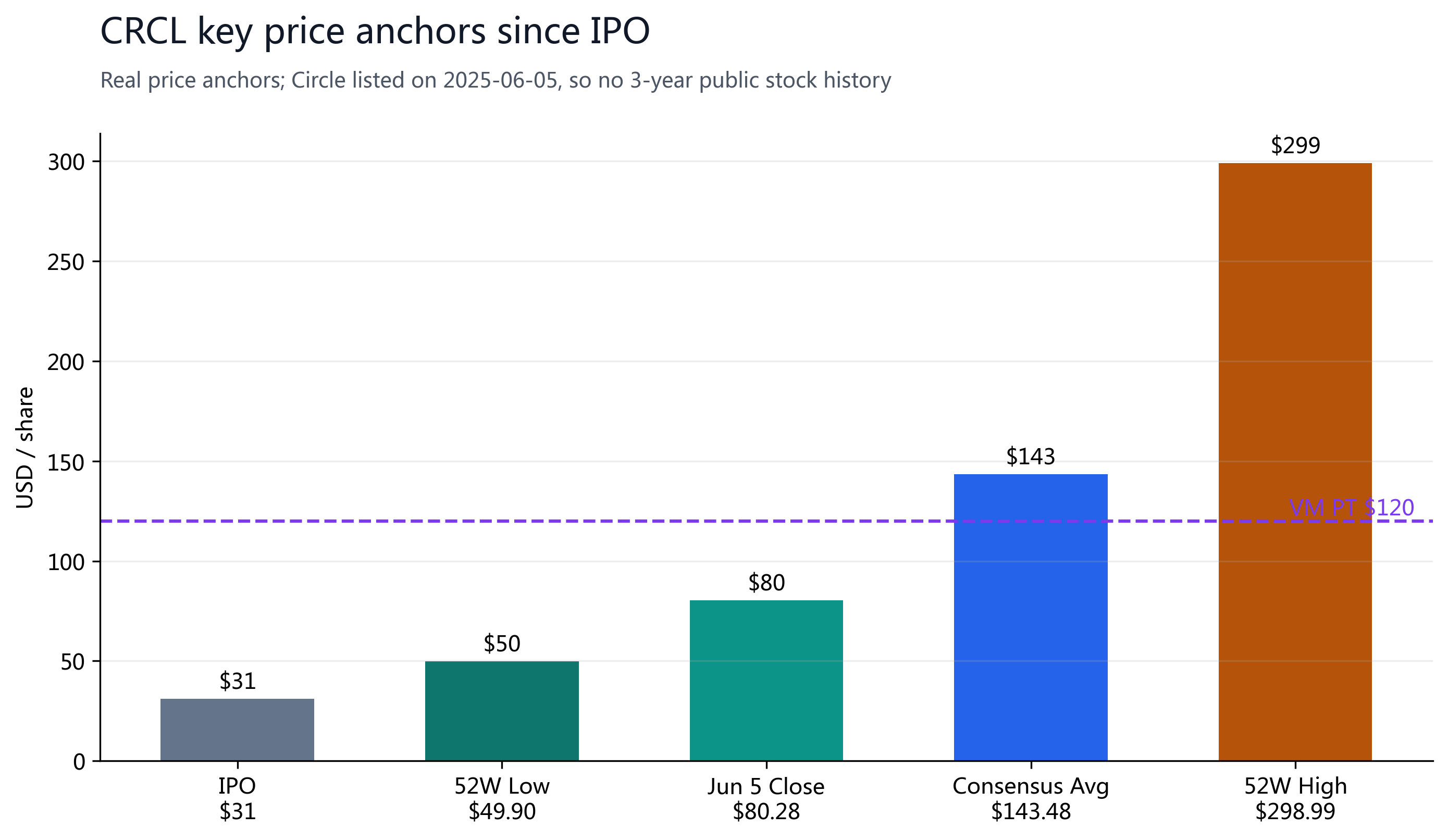

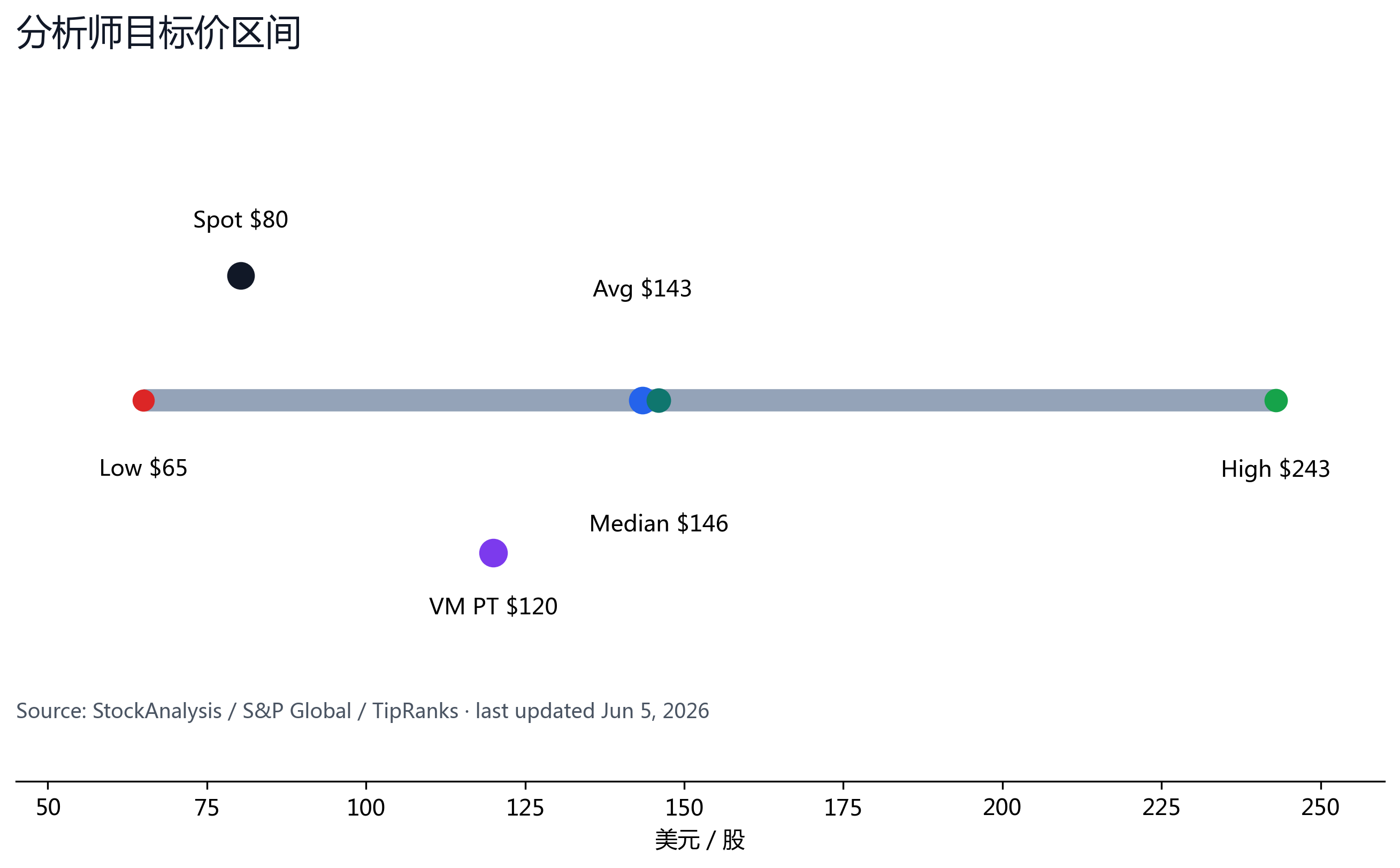

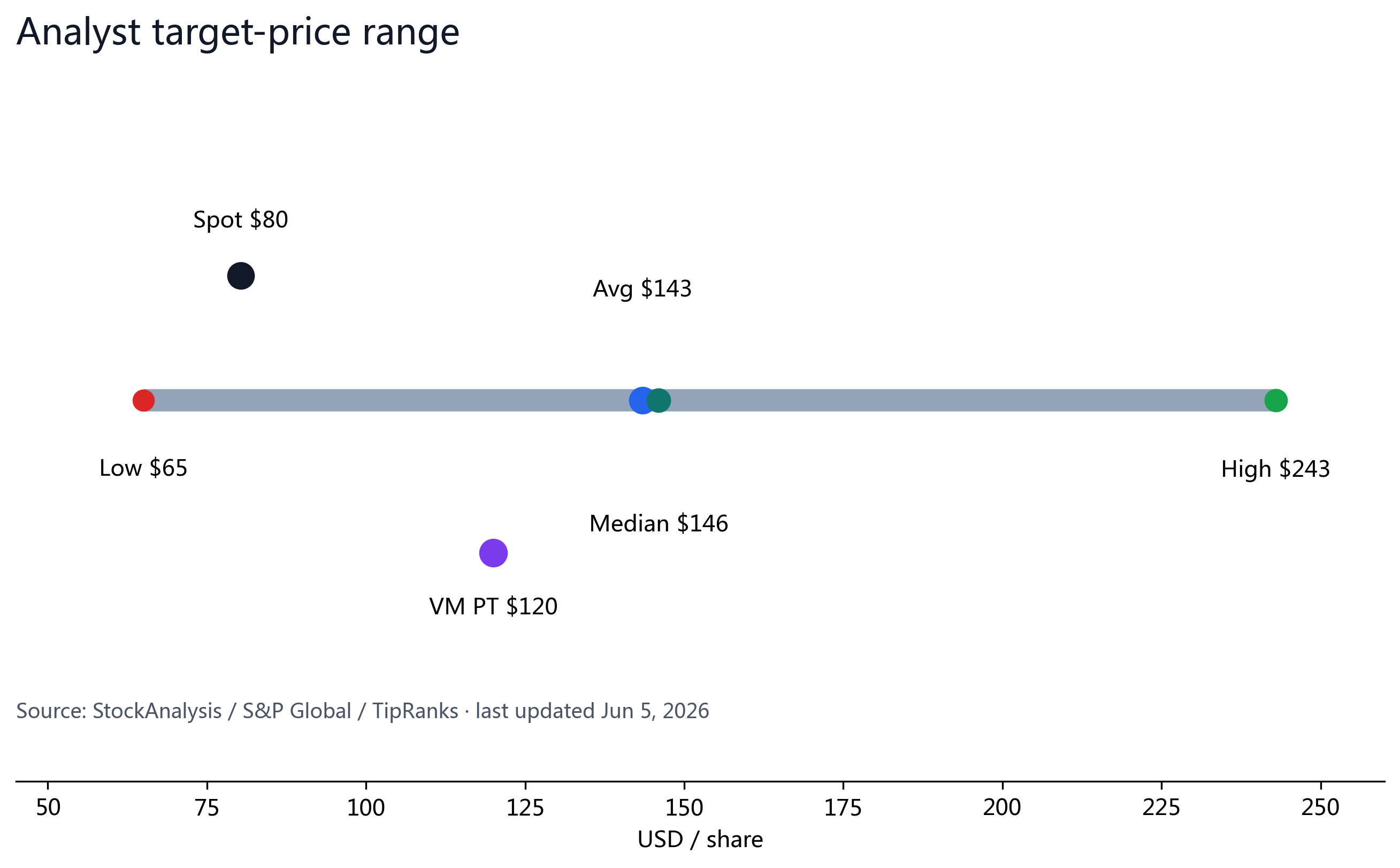

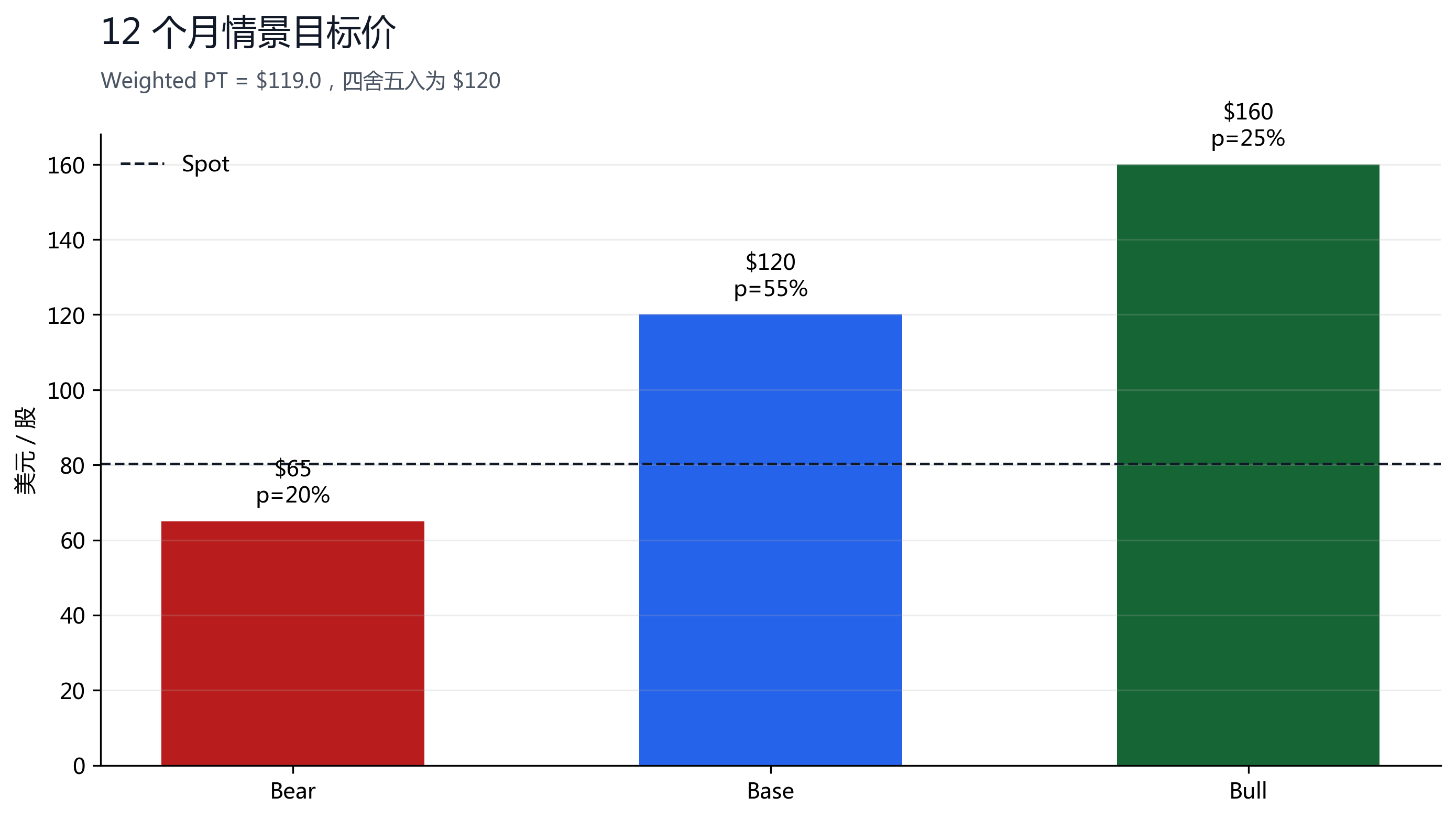

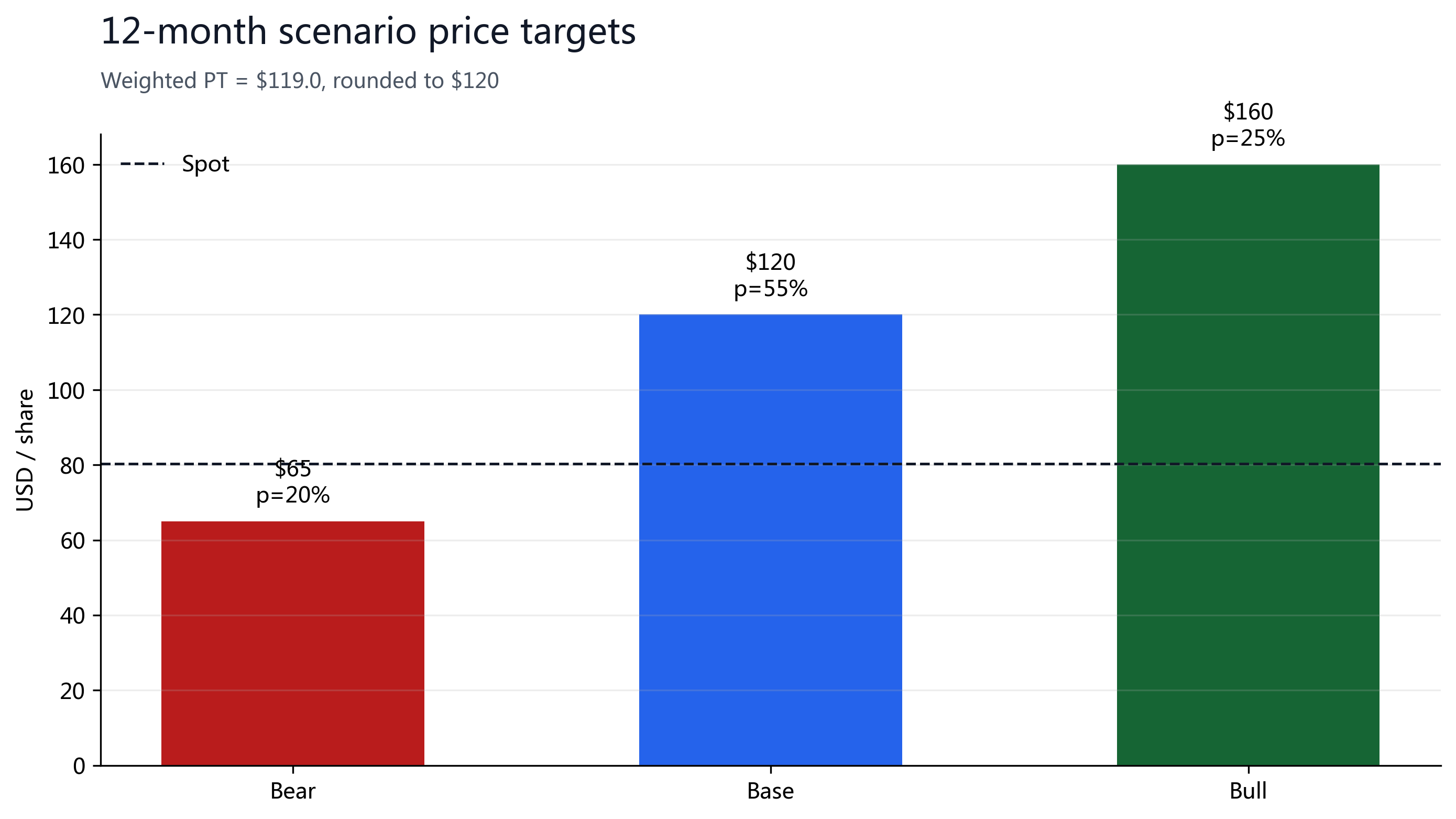

Report date 2026-06-08; market data cut is 2026-06-05 close. Circle is not a plain crypto exchange: it is a combination of USDC reserve economics, distribution network, and regulated payment infrastructure. The stock at $80.28 is below the 52W high of $298.99 by about -73%; CoinMarketCap's stablecoin page shows USDC at about $75.55B, Q1'26 total revenue and reserve income was $694M, and adjusted EBITDA was $151M. We rate CRCL Buy, with a 12-month price target of $120, implying +49.5% upside.

§01Investment Summary

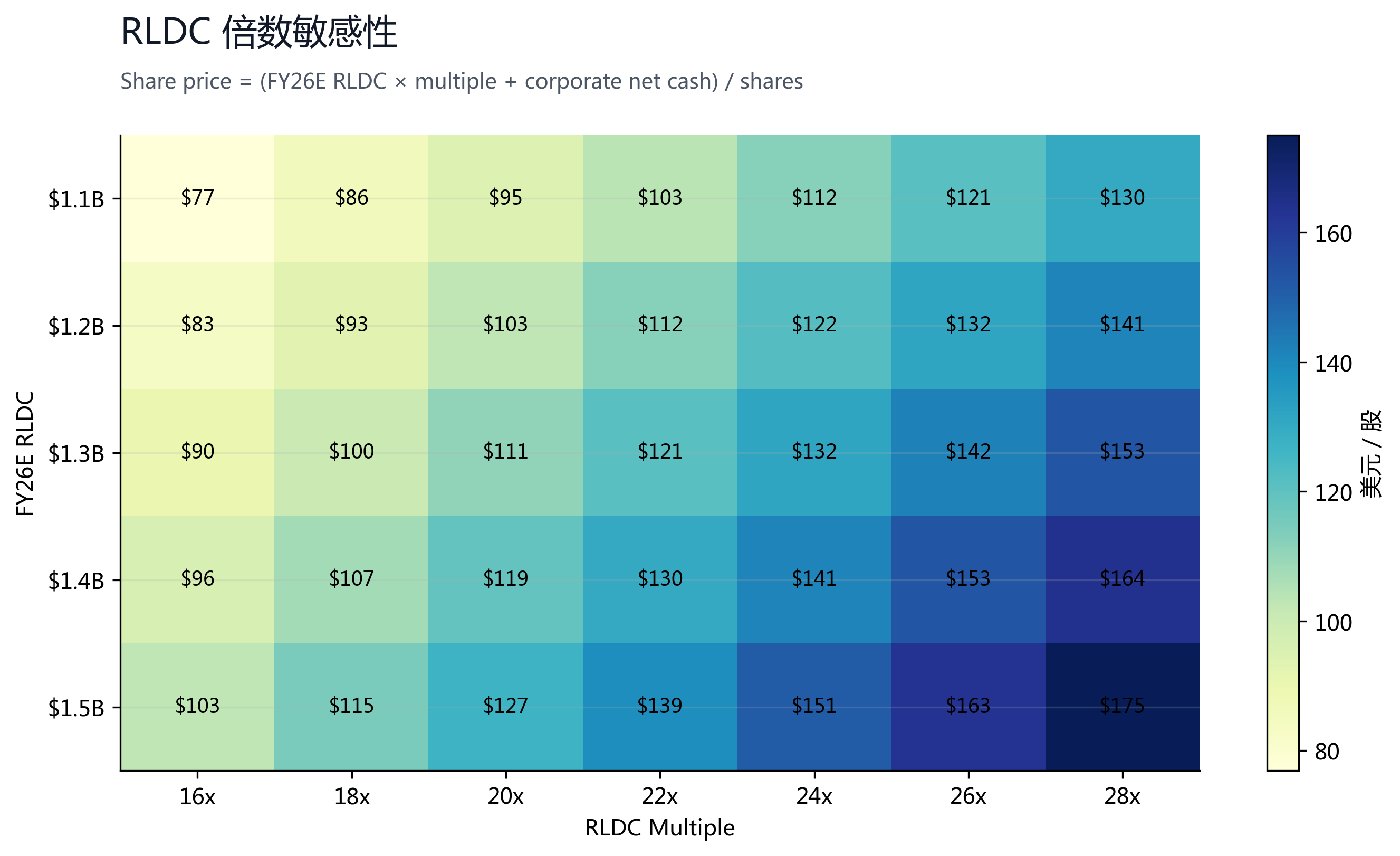

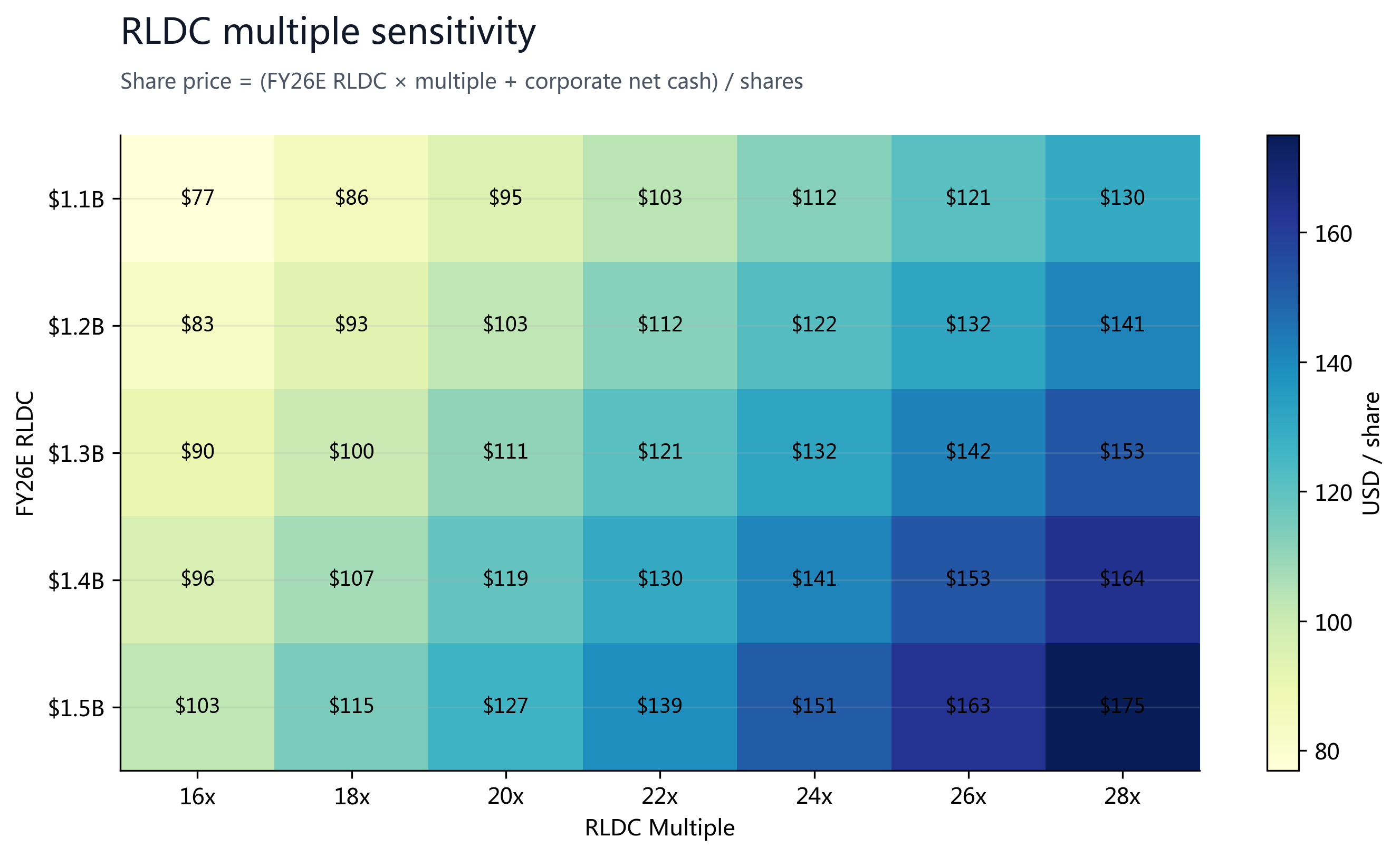

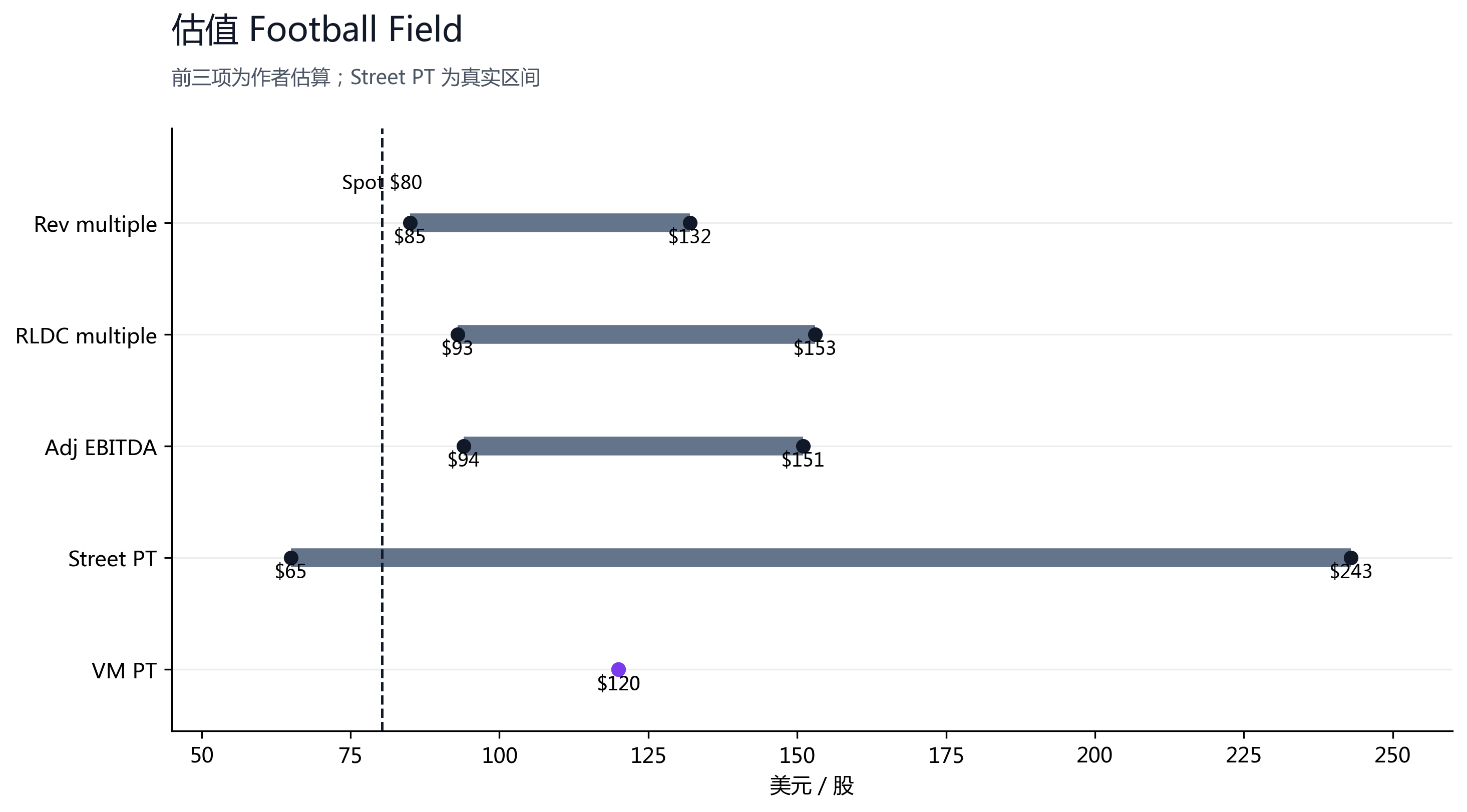

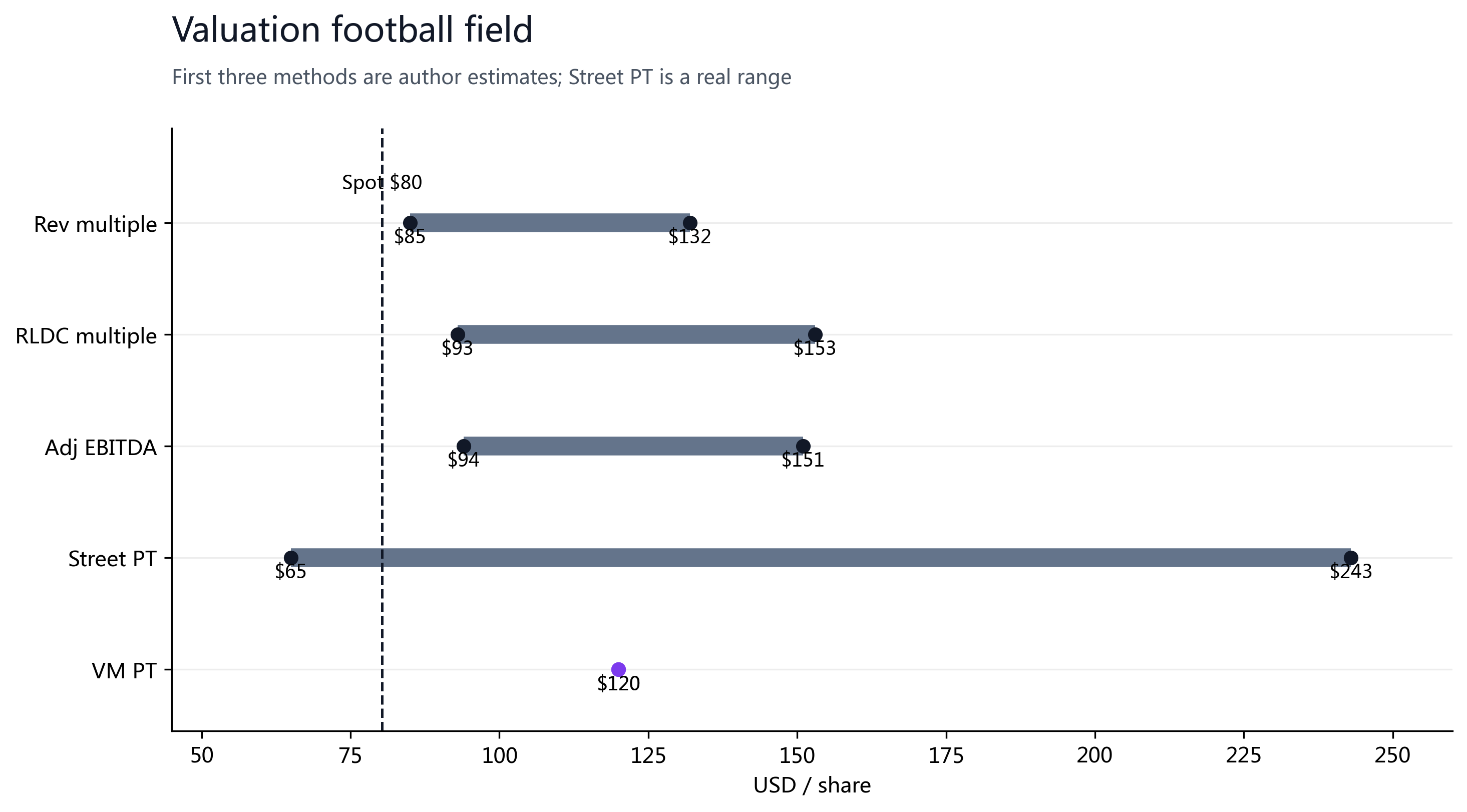

The core CRCL question is not whether crypto tokens go up; it is what multiple the market should pay for RLDC, or revenue contribution after distribution costs. RLDC means total revenue and reserve income less distribution, transaction and other costs, and it helps measure Circle's core revenue quality after distribution and transaction costs. We triangulate FY26E revenue, FY26E RLDC, FY26E adjusted EBITDA, and then cross-check against Street target prices. The weighted result is $119, rounded to a 12-month price target of $120.

§02Price and Street View

| Metric | Value | Source / Note |

|---|---|---|

| Current price | $80.28 | StockAnalysis · Jun 5 close |

| Market cap | $19.96B | StockAnalysis |

| Shares outstanding | 248.58M | StockAnalysis |

| 52W range | $49.90-$298.99 | StockAnalysis |

| Analyst PT | $65 / $143.48 / $146 / $243 | Low / Avg / Median / High · S&P Global via StockAnalysis |

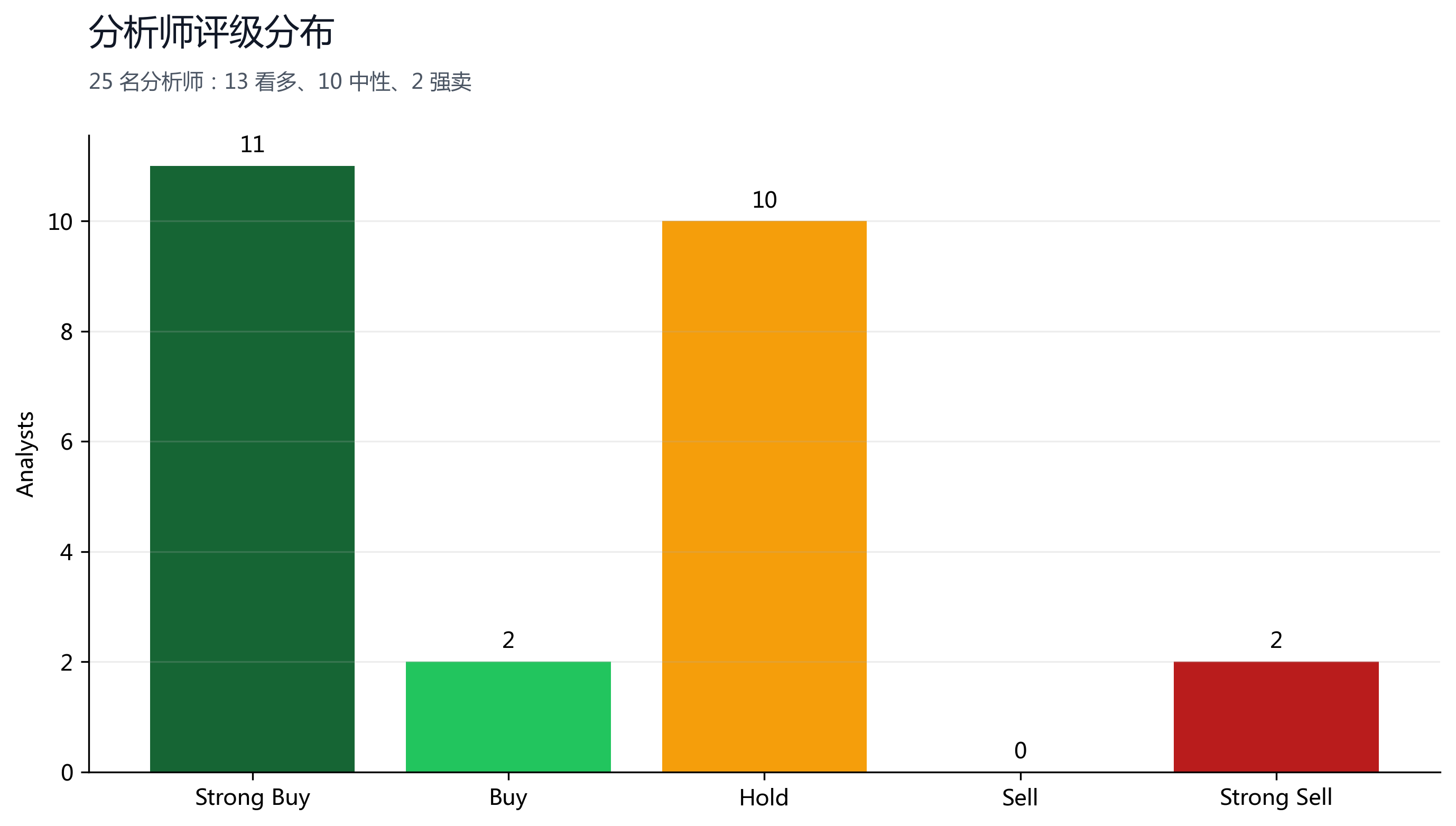

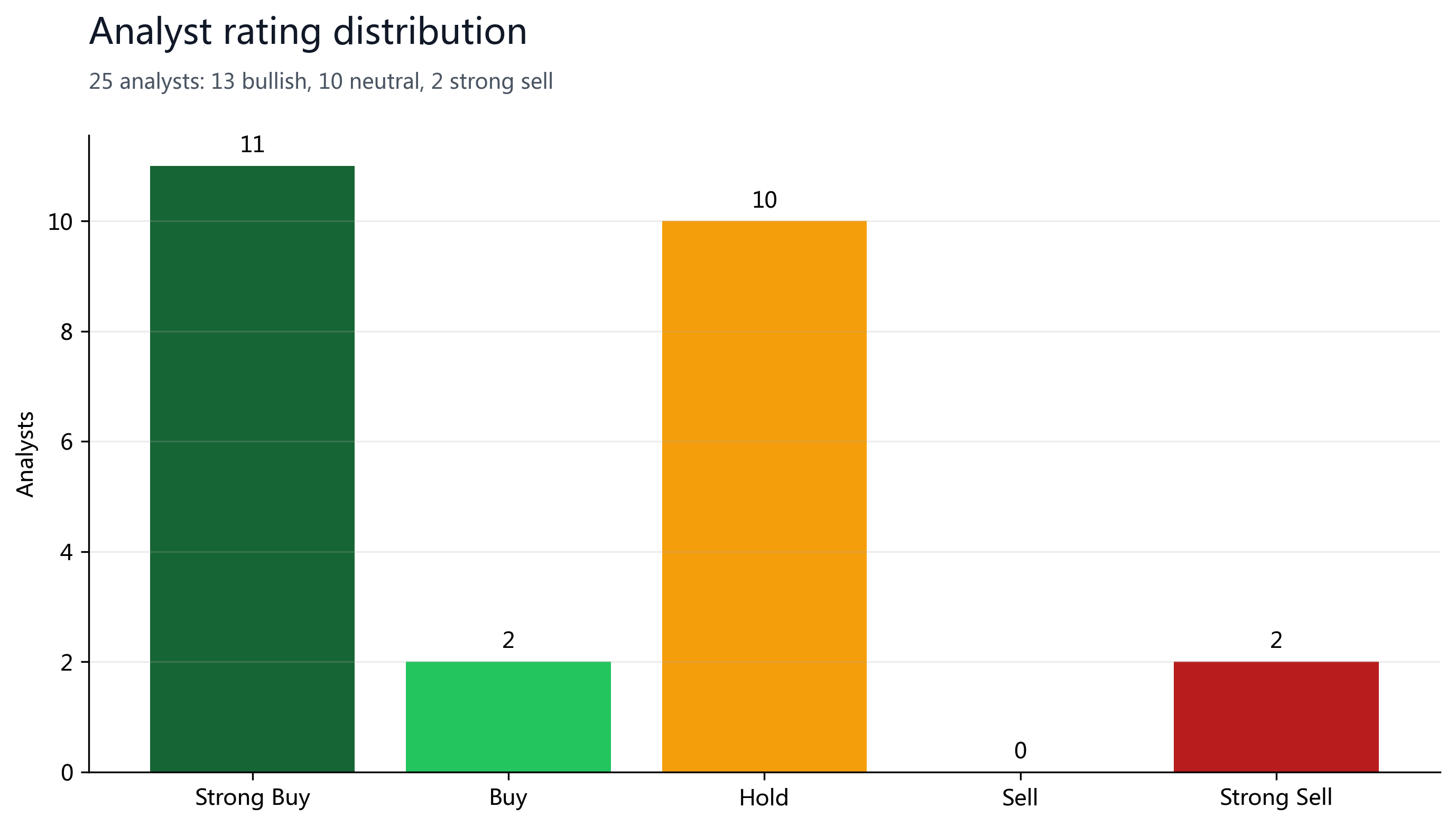

| Recommendation split | 11 / 2 / 10 / 0 / 2 | Strong Buy / Buy / Hold / Sell / Strong Sell |

§03Bull/Bear View

Bull case: scarce public regulated-stablecoin exposure

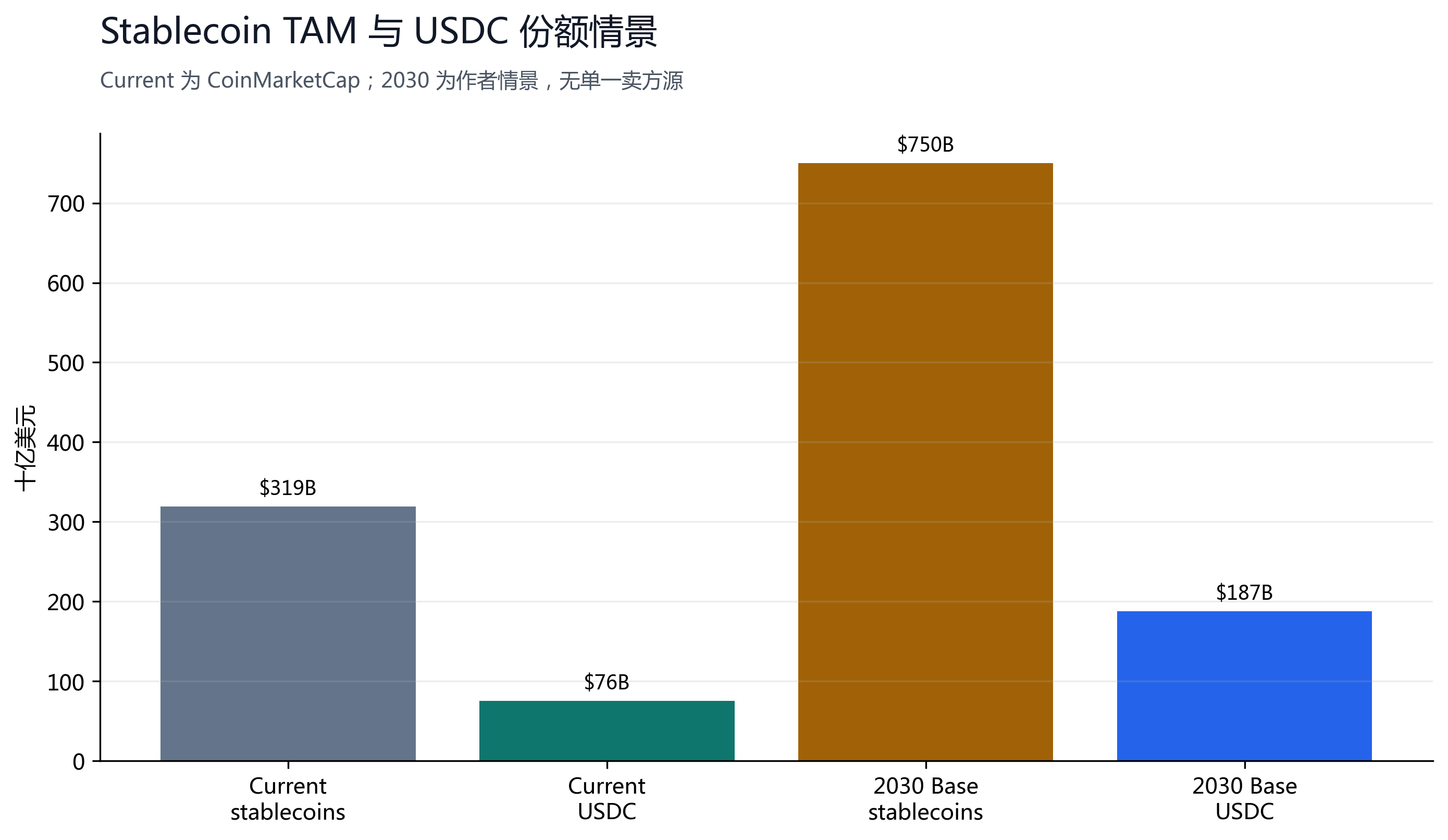

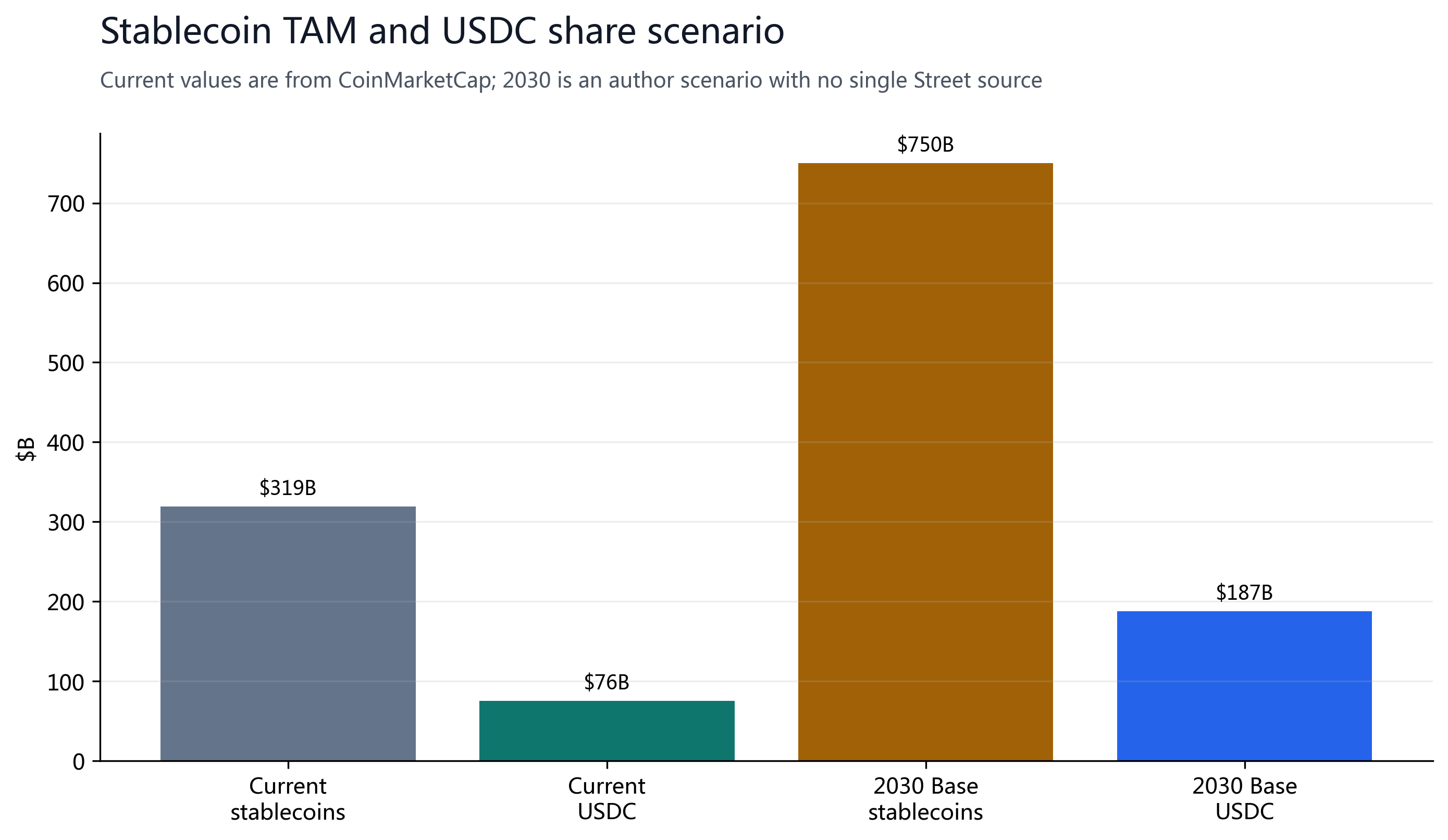

Circle is the issuer and infrastructure company behind USDC; CoinMarketCap's stablecoin page is a public page tracking the market value of stablecoins such as USDT and USDC, showing total stablecoin market cap of about $318.93B, USDC at $75.55B, and USDT at $187.47B. CRCL gives investors one of the few direct public-equity ways to own stablecoin reserve economics plus payment-network growth.

Bear case: reserve income is not software ARR; rates and distribution costs are hard constraints

Circle's revenue depends heavily on reserve yields and USDC circulation, while distribution costs are tied to exchanges, wallets, and payment-platform bargaining power. If 3M/10Y rates fall, Coinbase's leverage increases, or Visa/Mastercard/Stripe launch competing networks, CRCL deserves a lower multiple than traditional payment networks.

§04Financial Truth

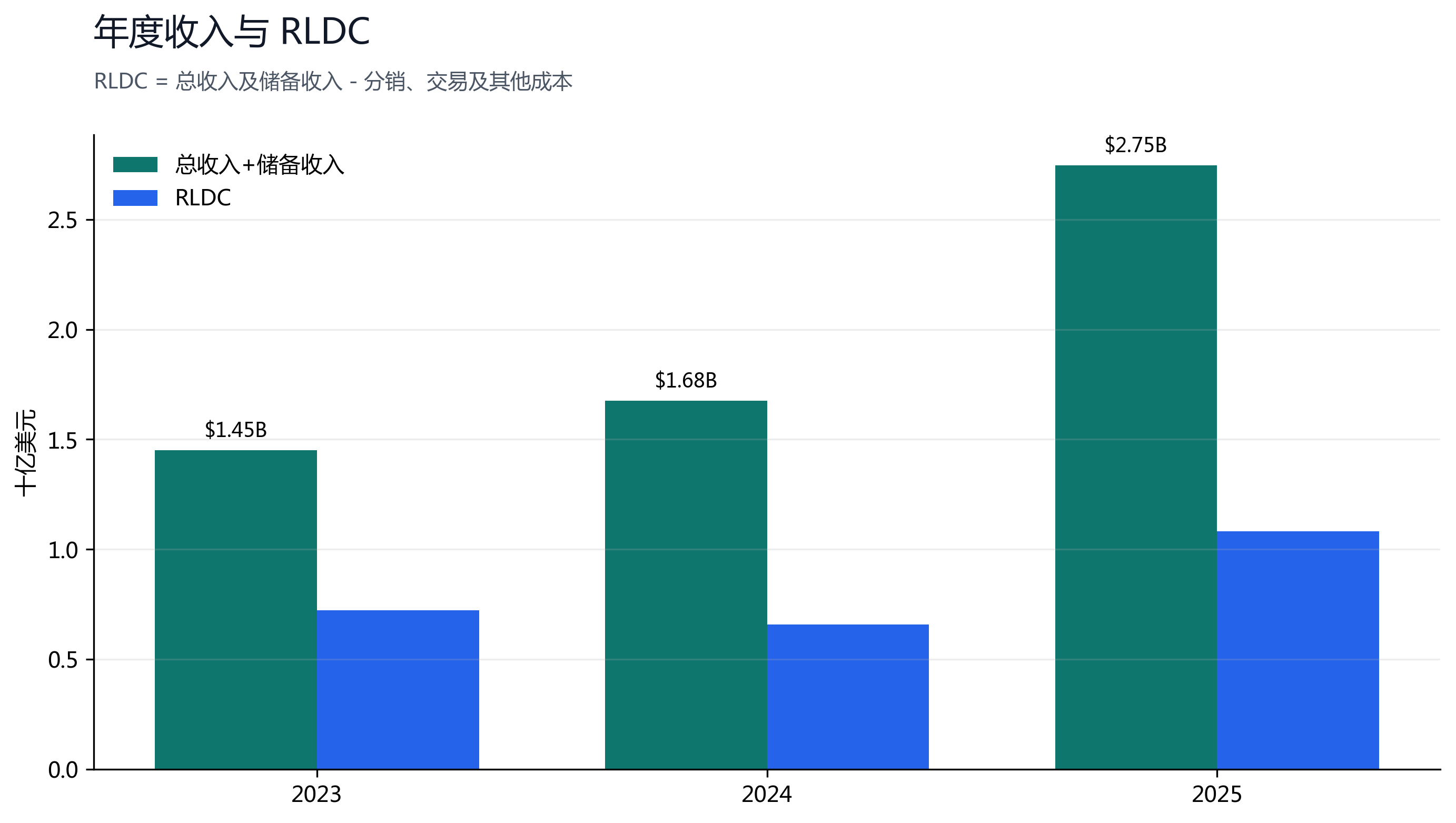

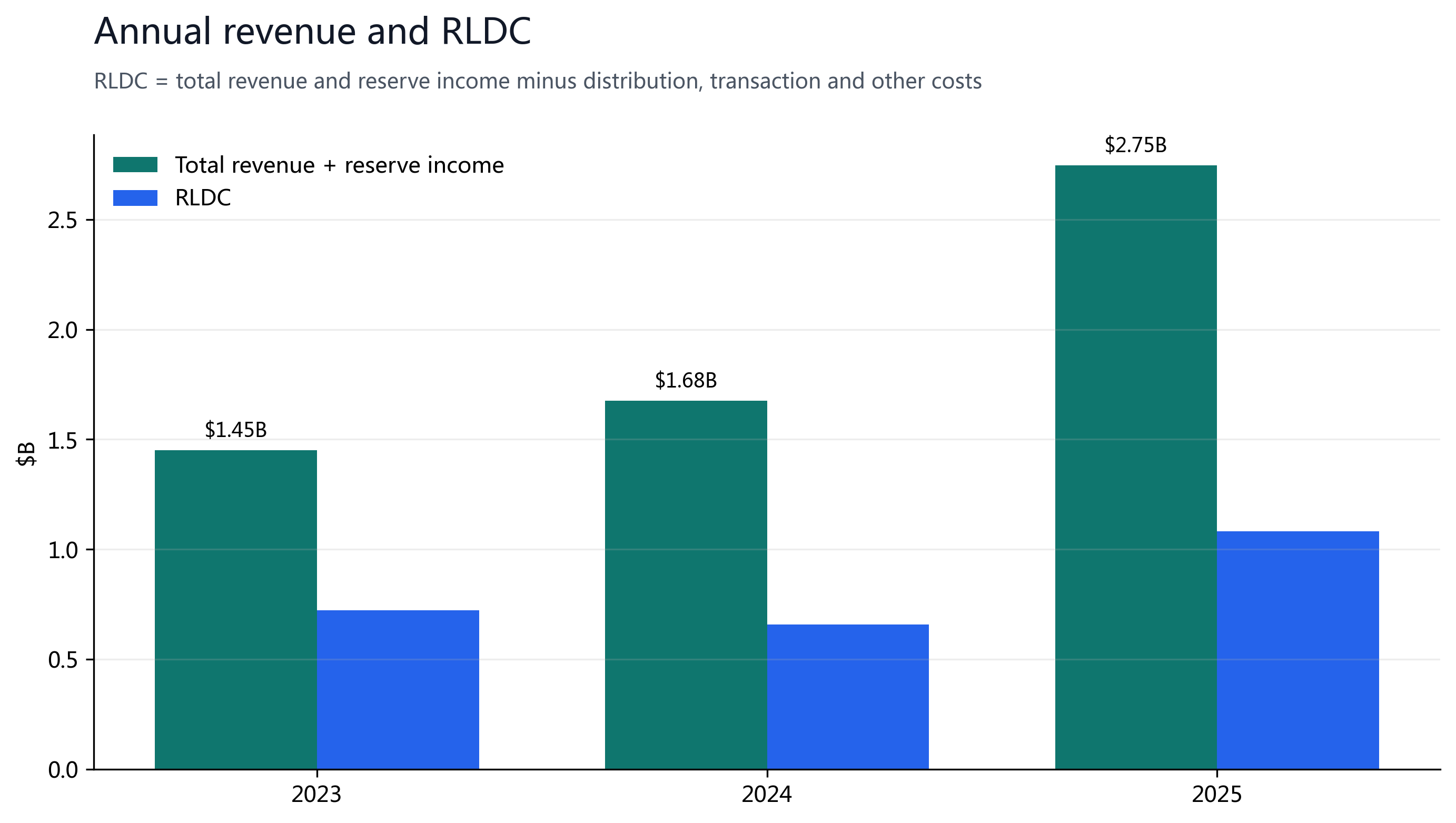

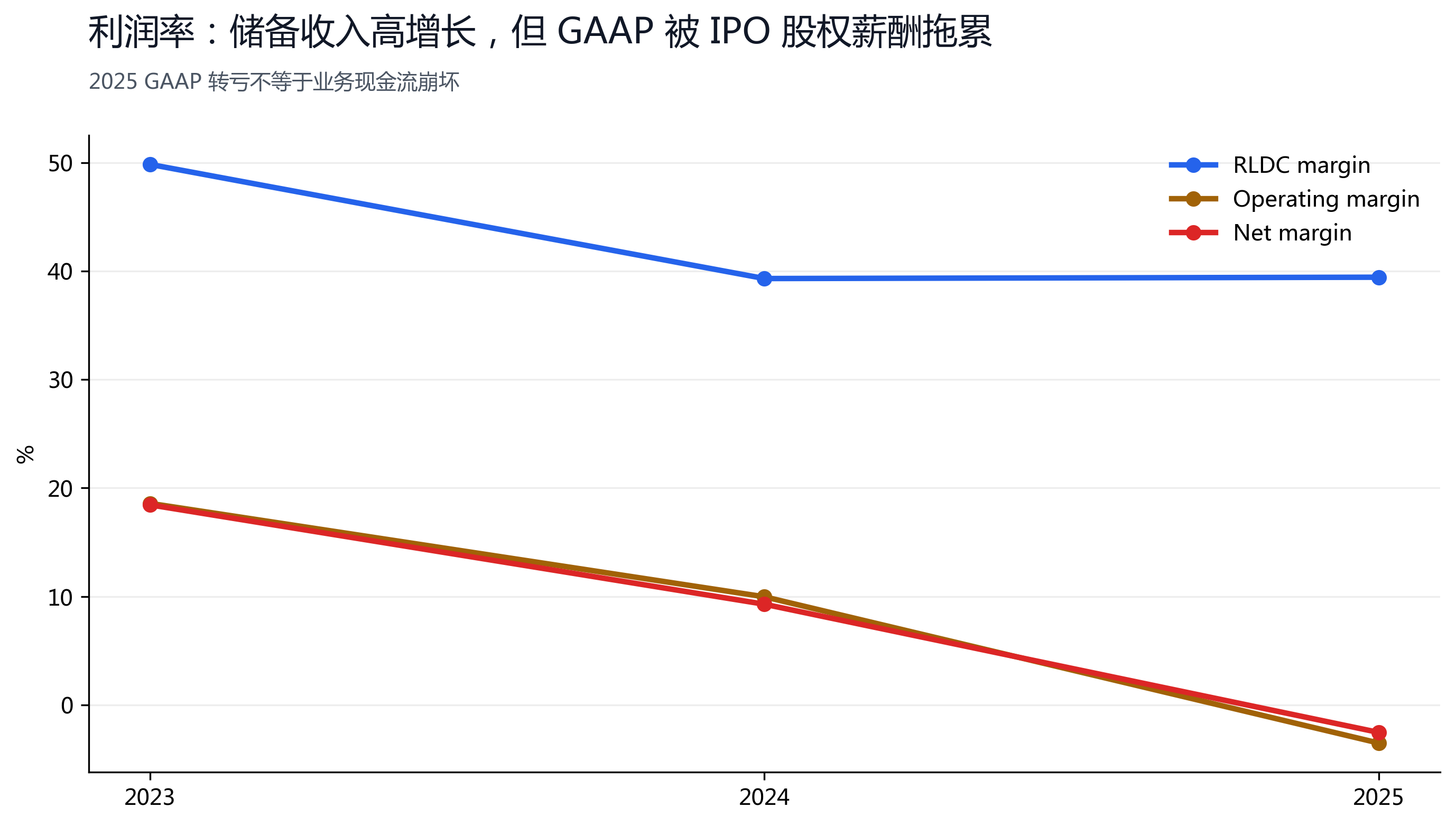

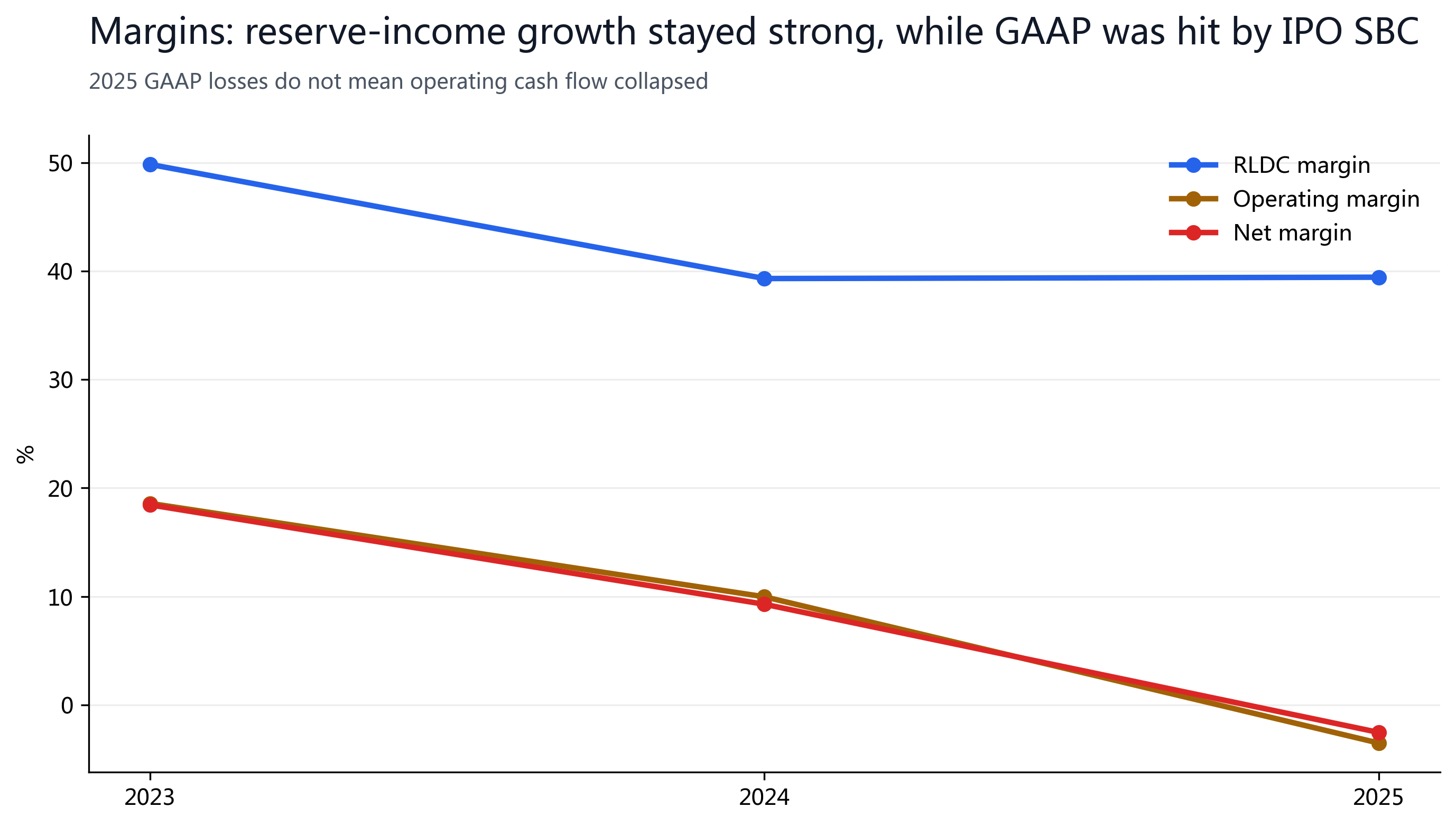

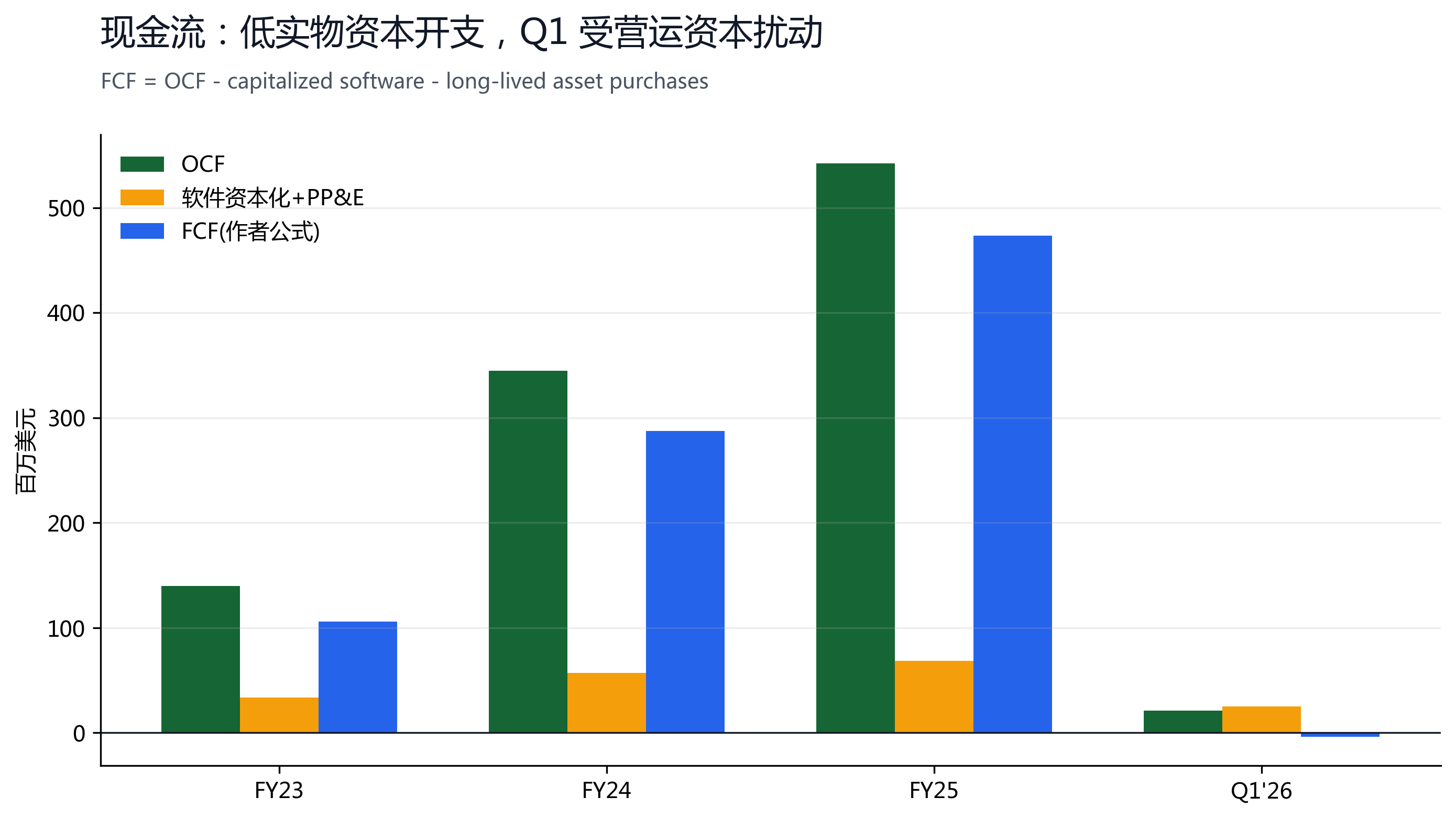

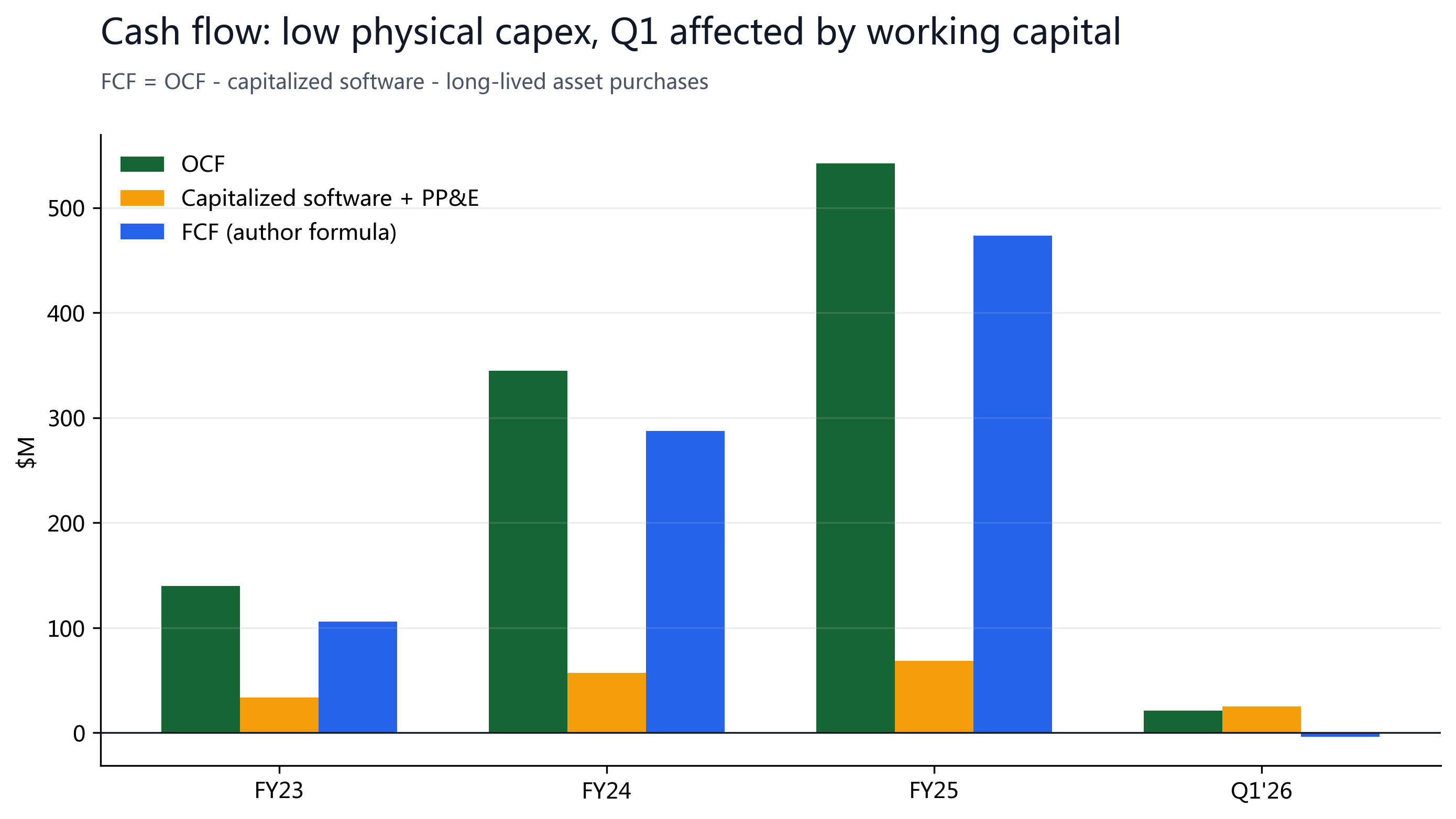

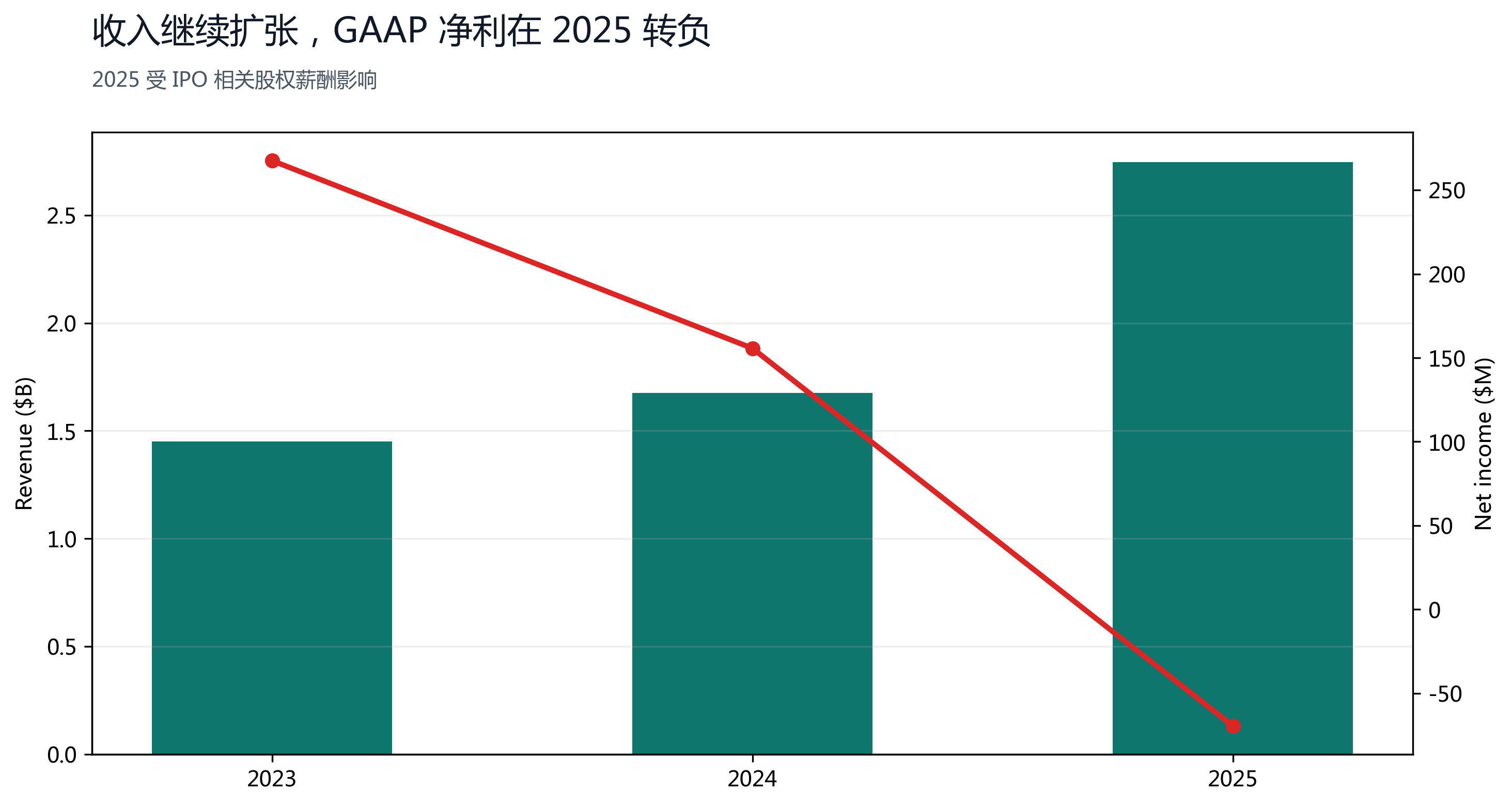

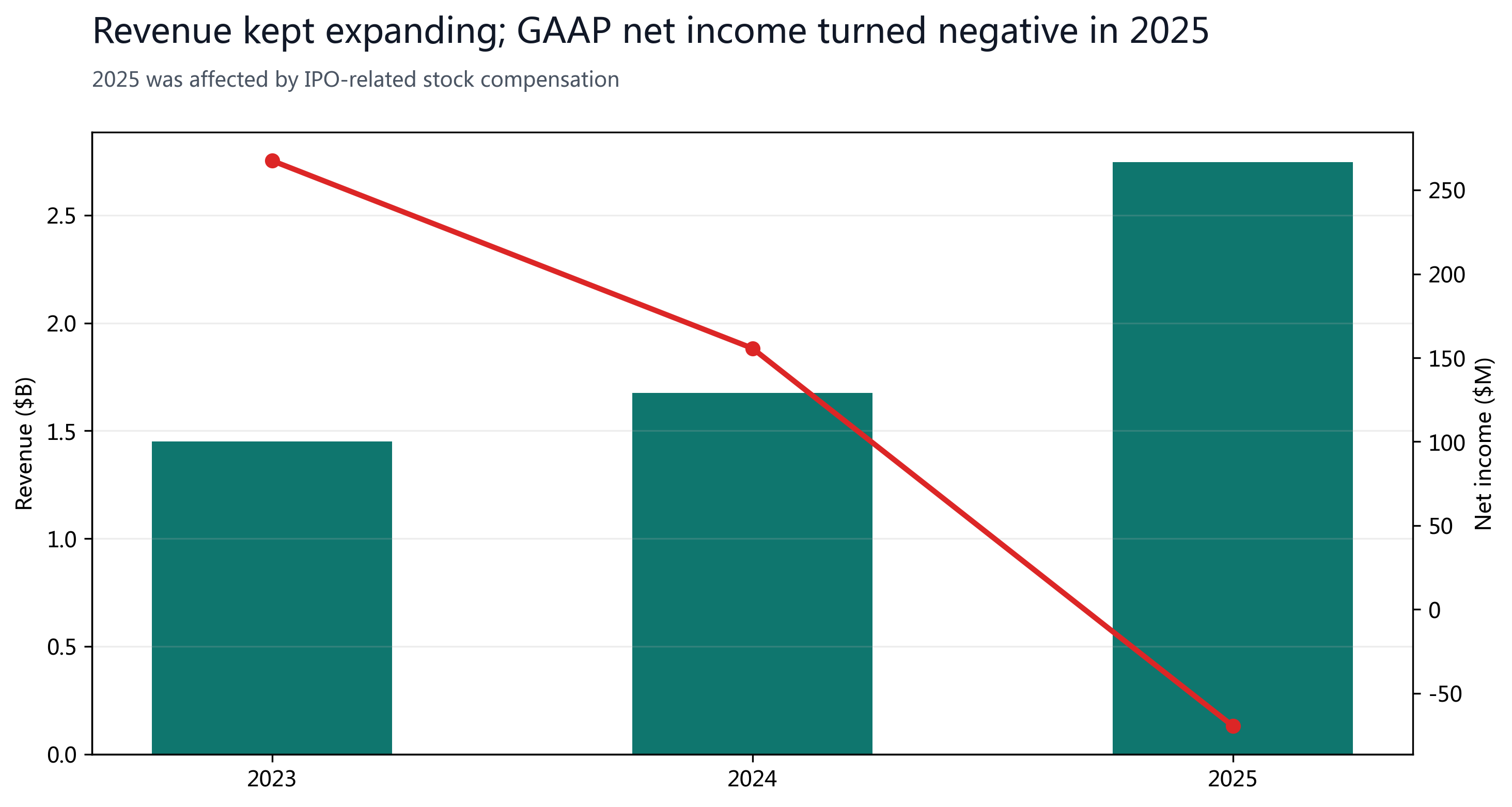

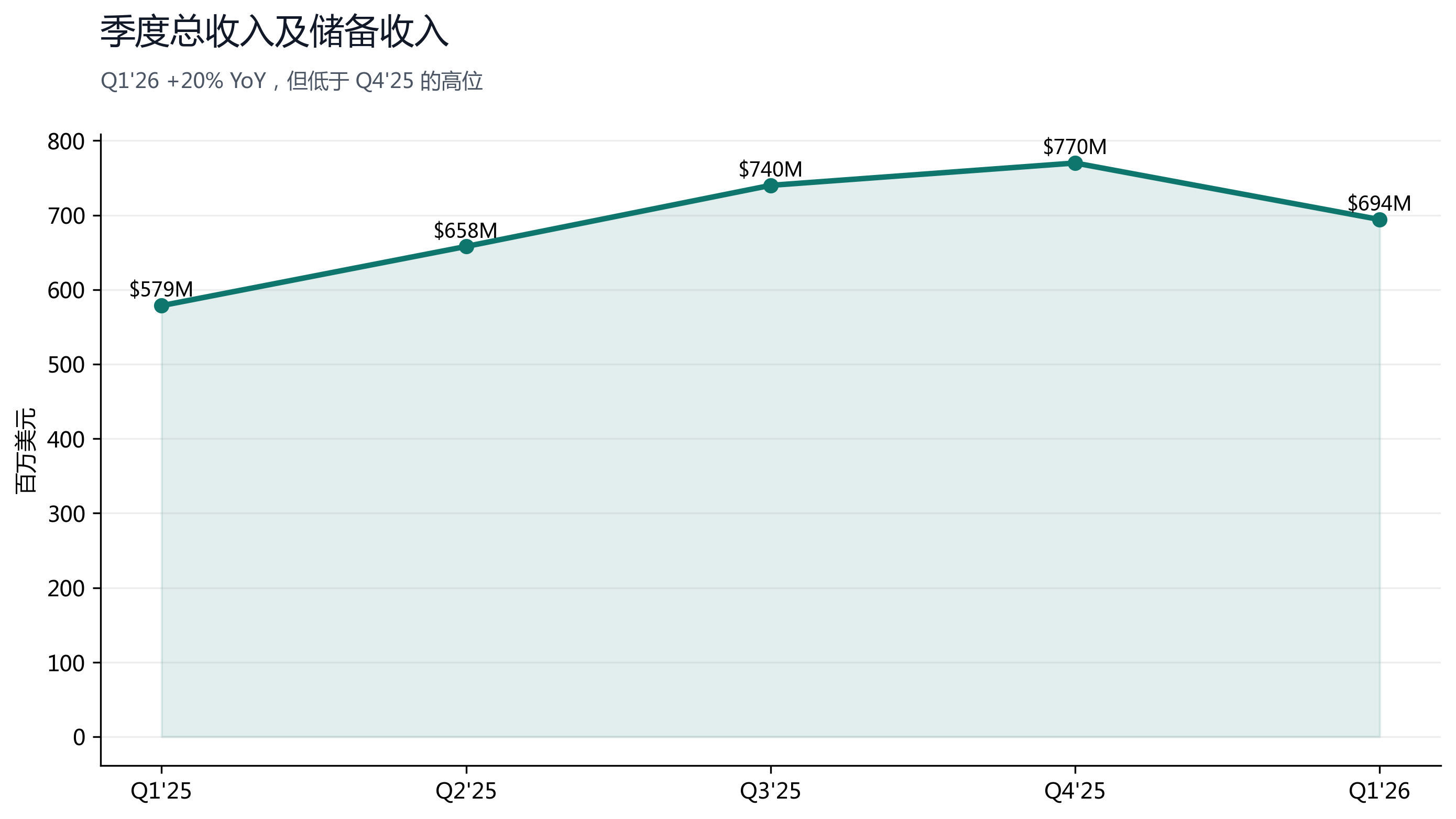

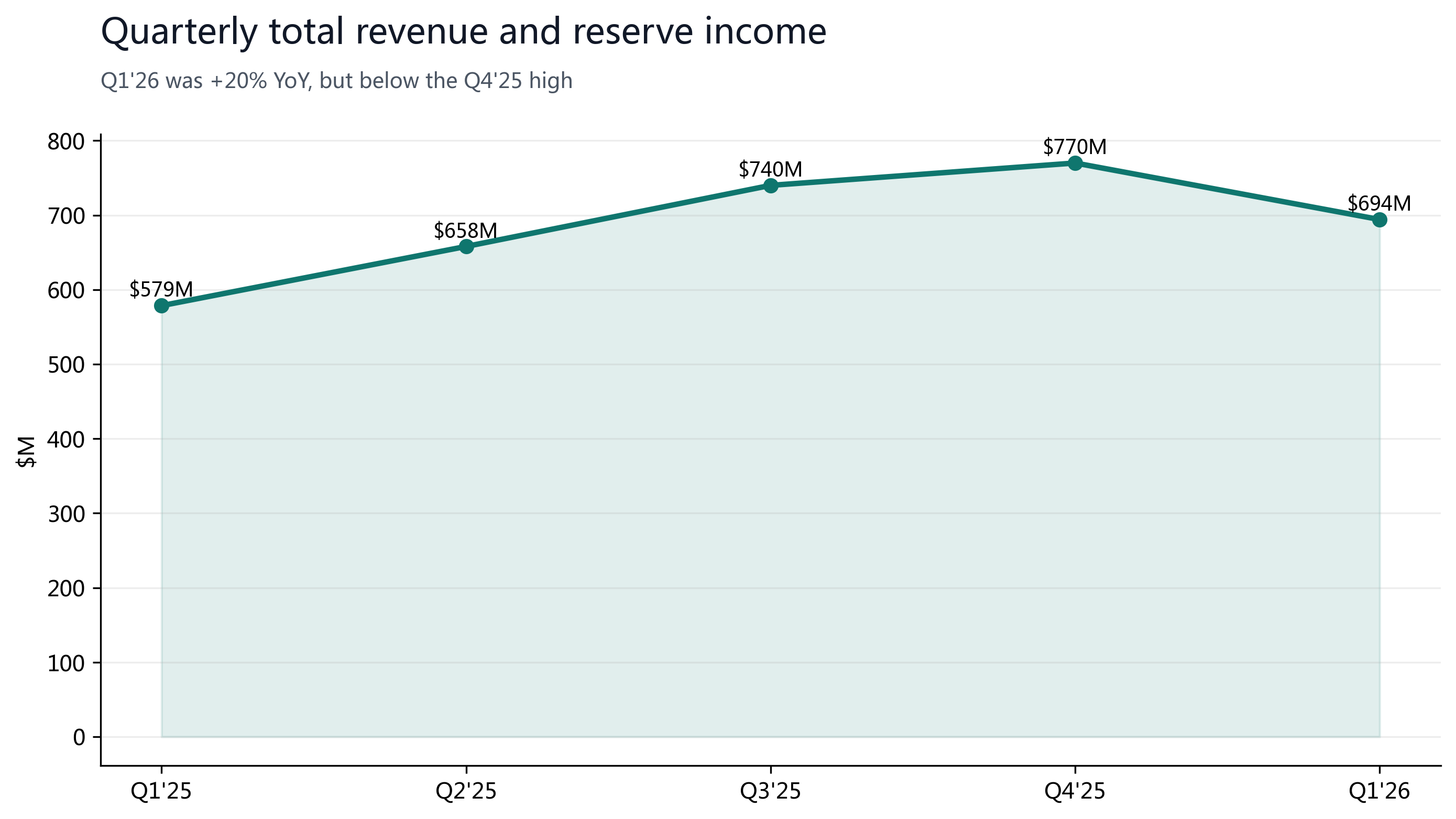

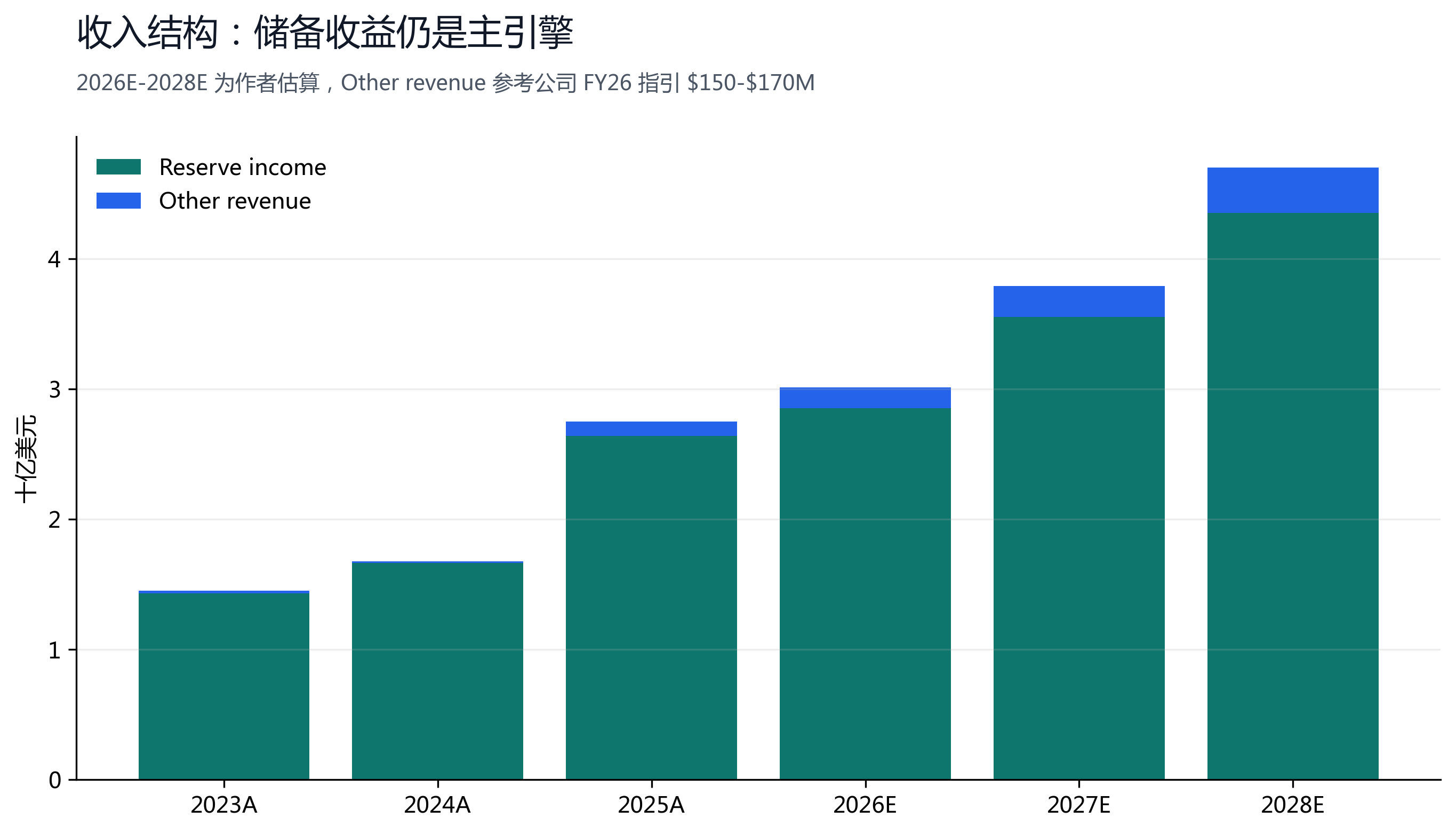

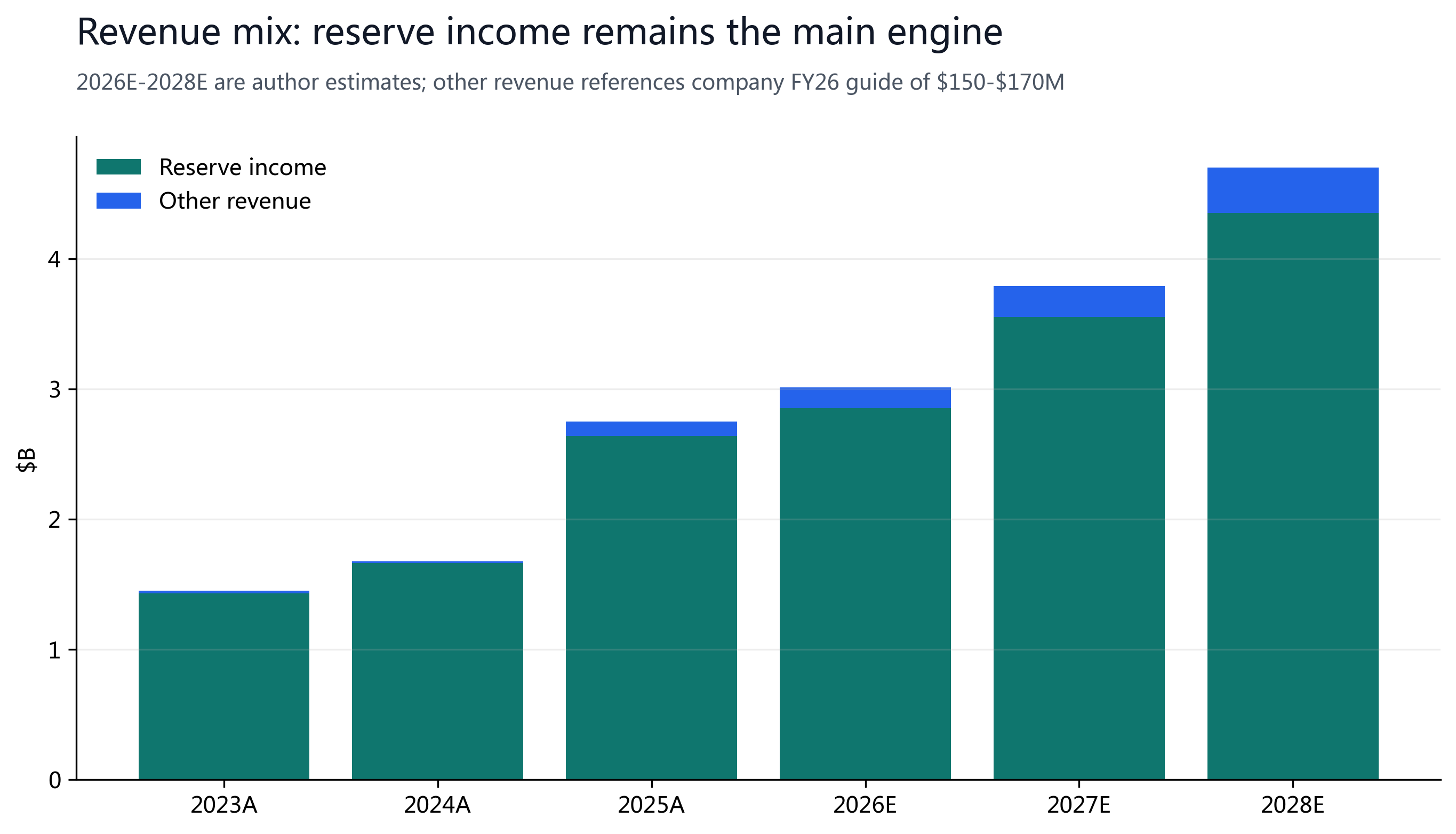

FY2025 total revenue and reserve income was $2.747B, up 64%; RLDC, or revenue contribution after distribution, transaction and other related costs, was $1.083B with a 39% RLDC margin. GAAP net loss was $69.5M, mainly affected by IPO-related stock compensation; adjusted EBITDA was $582M, up 104%. Q1'26 total revenue and reserve income was $694M, up 20%; net income was $55M, down 15%; adjusted EBITDA was $151M, up 24%.

| Metric | 2023 | 2024 | 2025 | Q1'26 |

|---|---|---|---|---|

| Total revenue + reserve income | $1.450B | $1.676B | $2.747B | $694M |

| RLDC | $723M | $659M | $1.083B | $287M |

| Net income | $268M | $156M | -$69.5M | $55M |

| OCF | $140M | $345M | $542M | $21M |

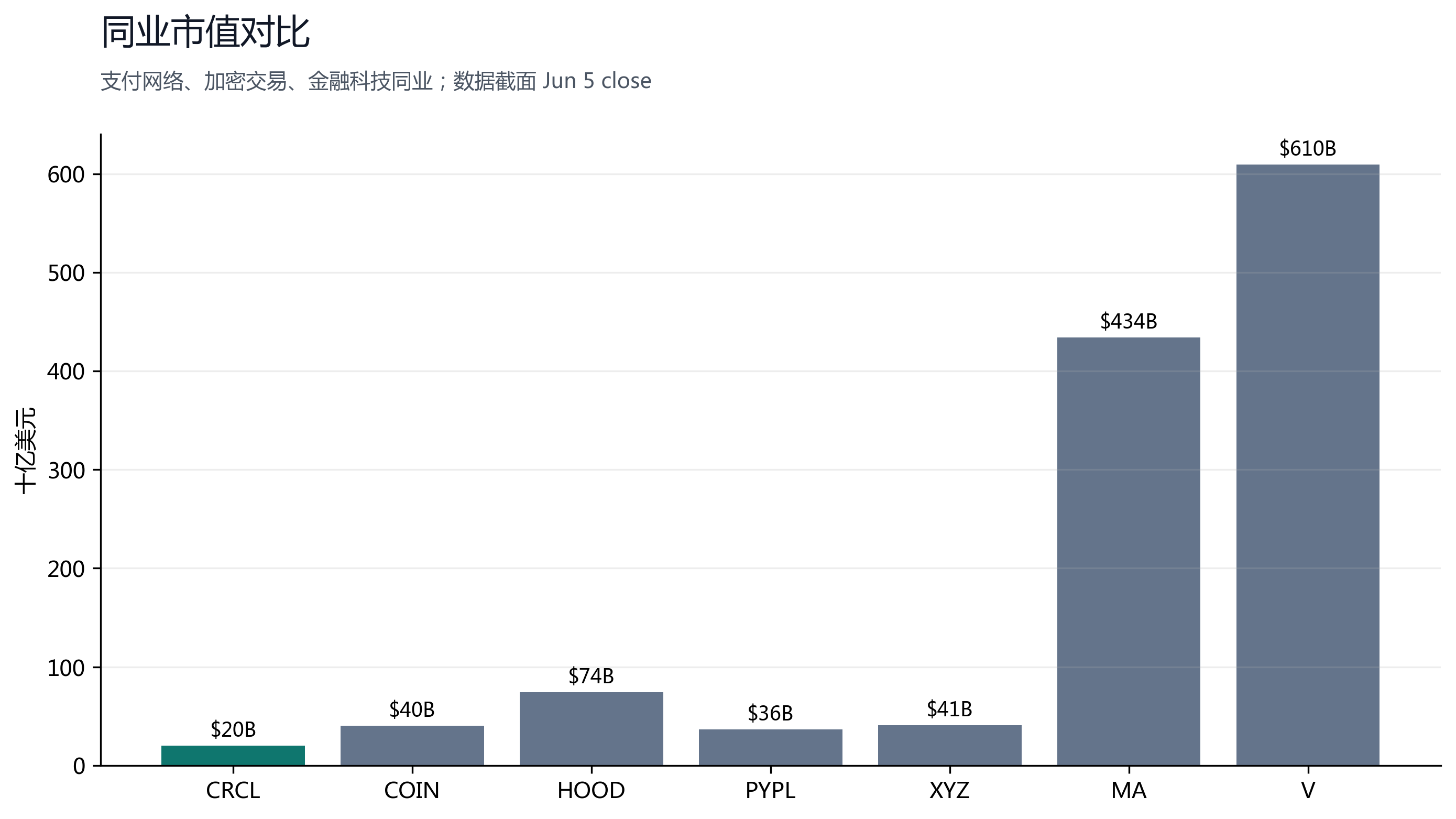

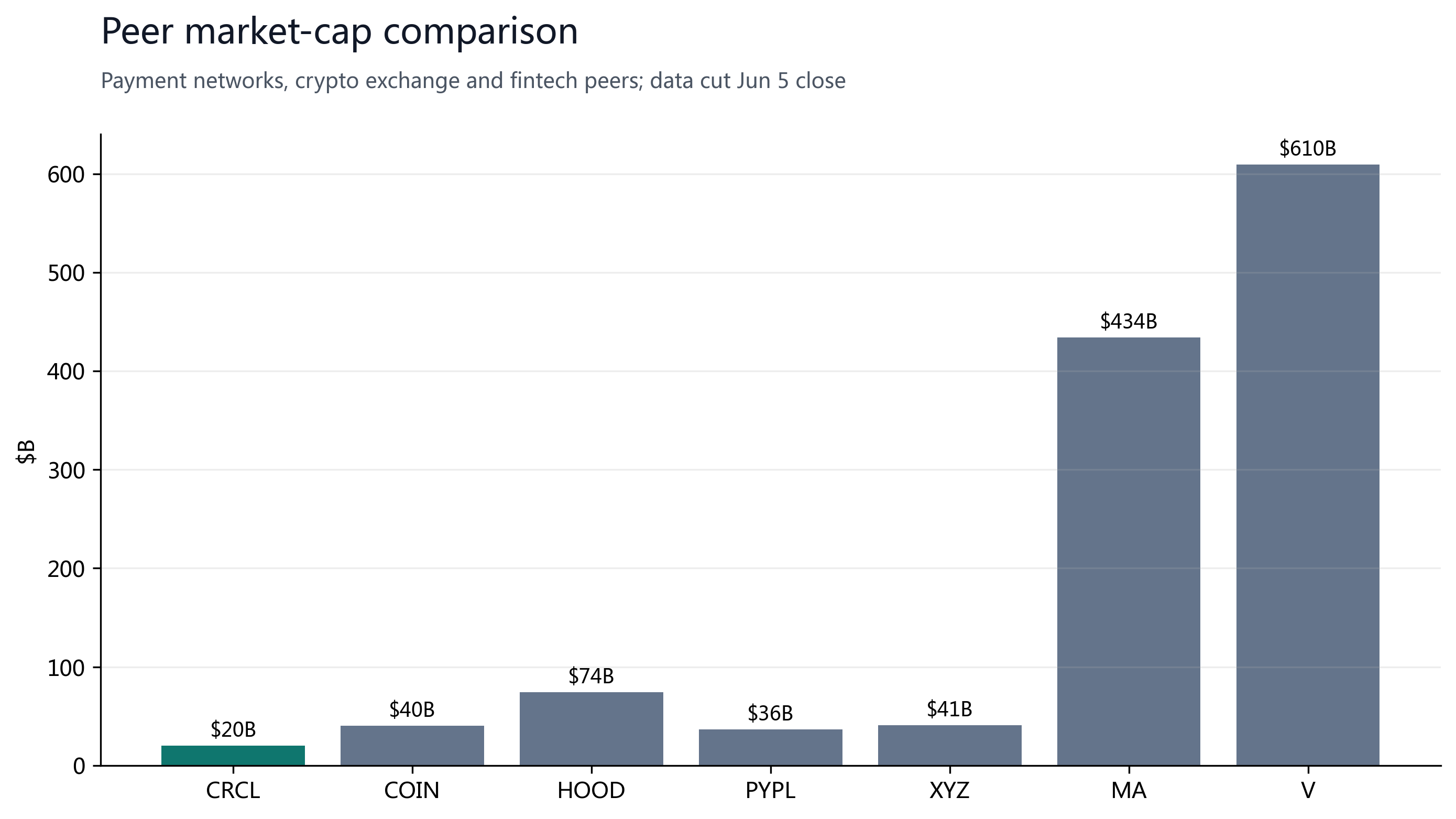

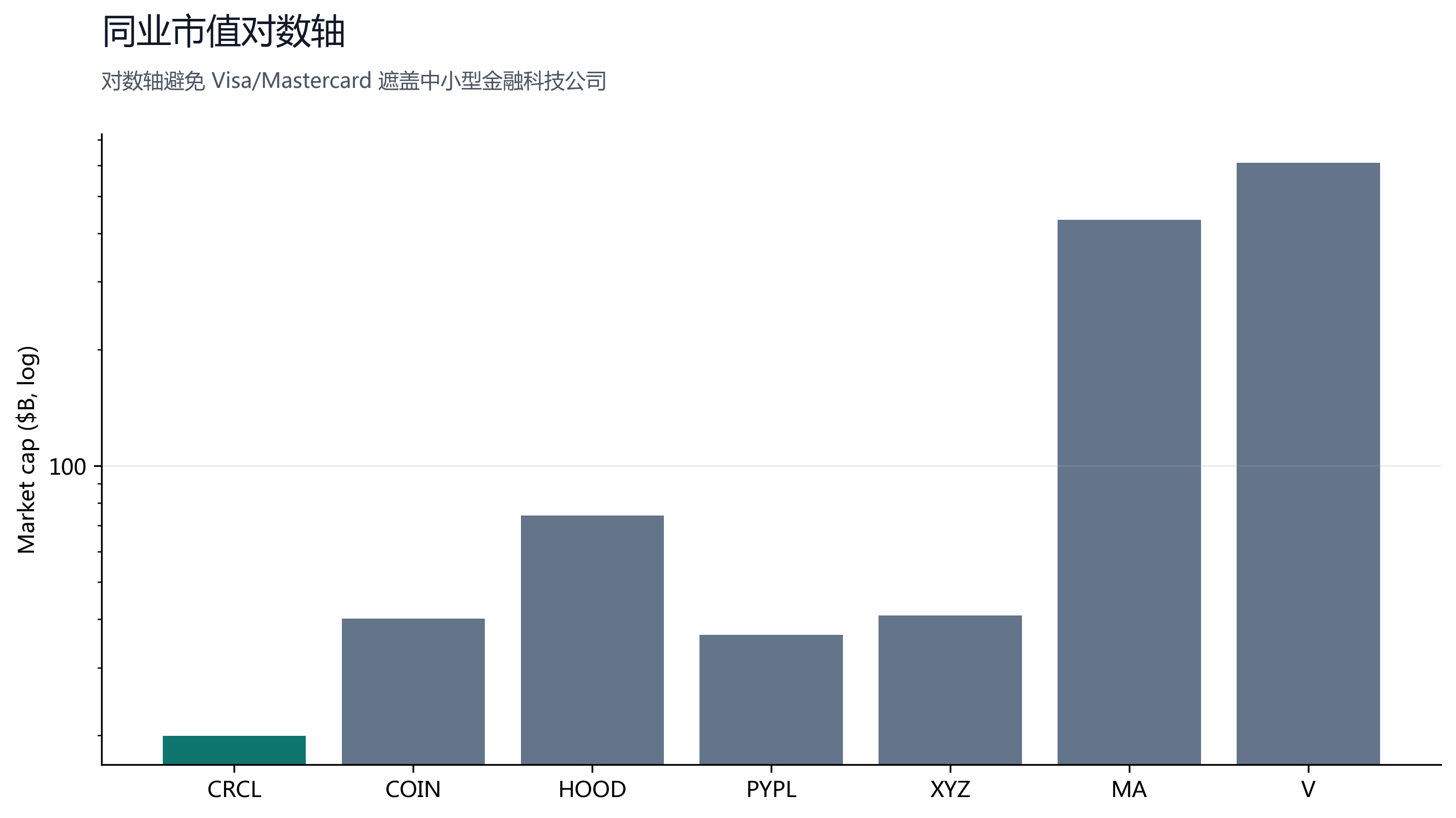

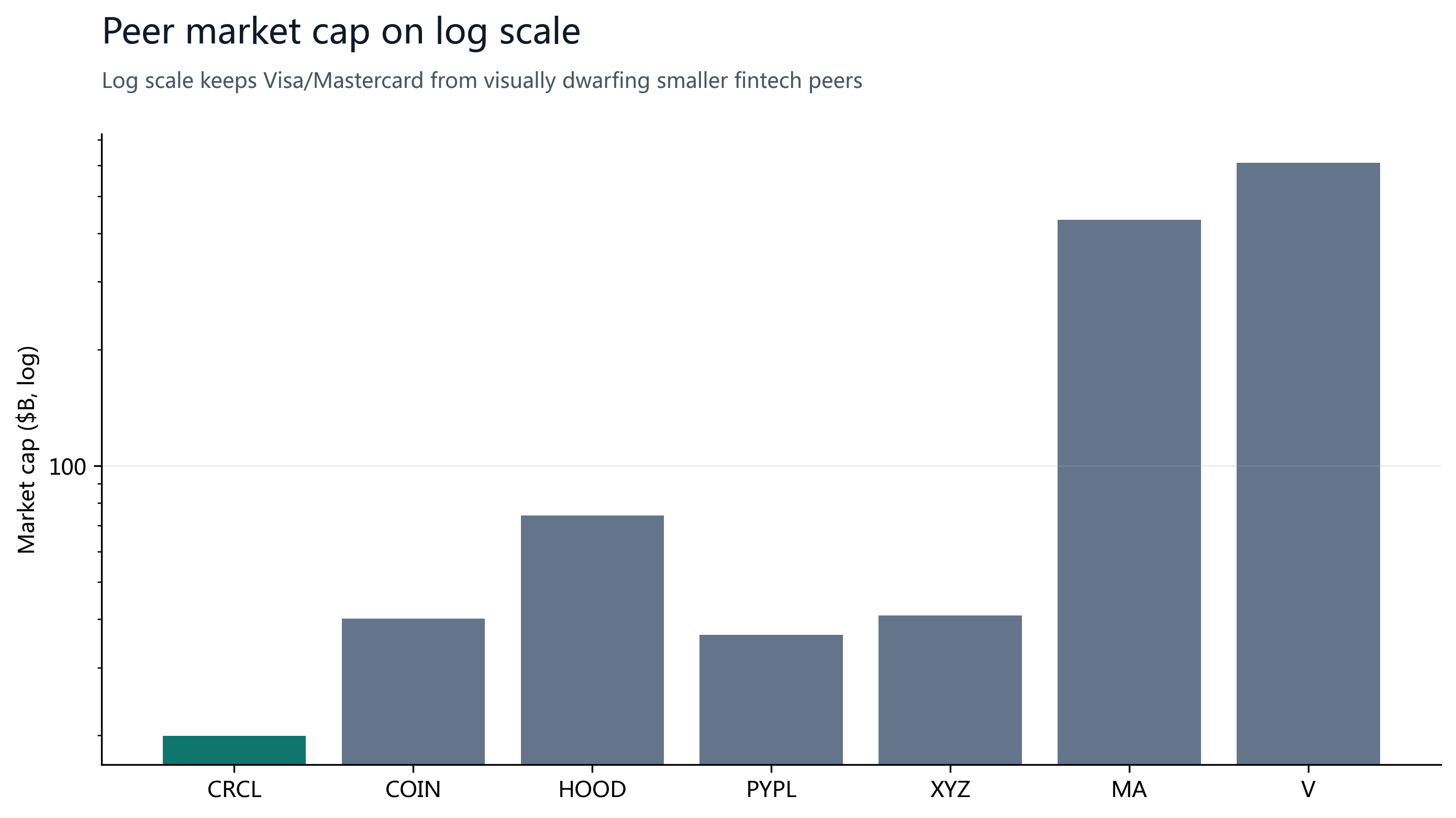

§05Peer Comparables

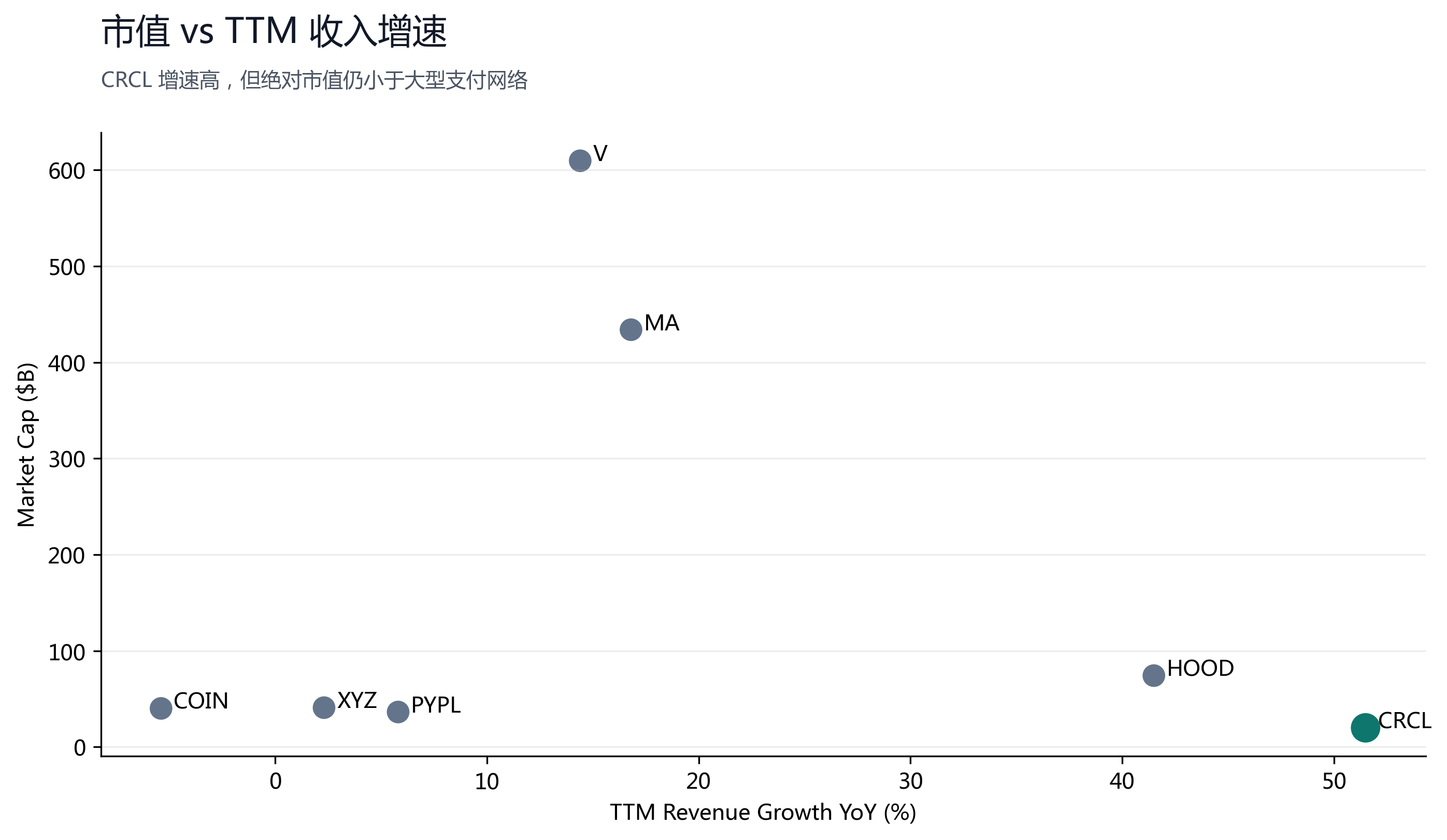

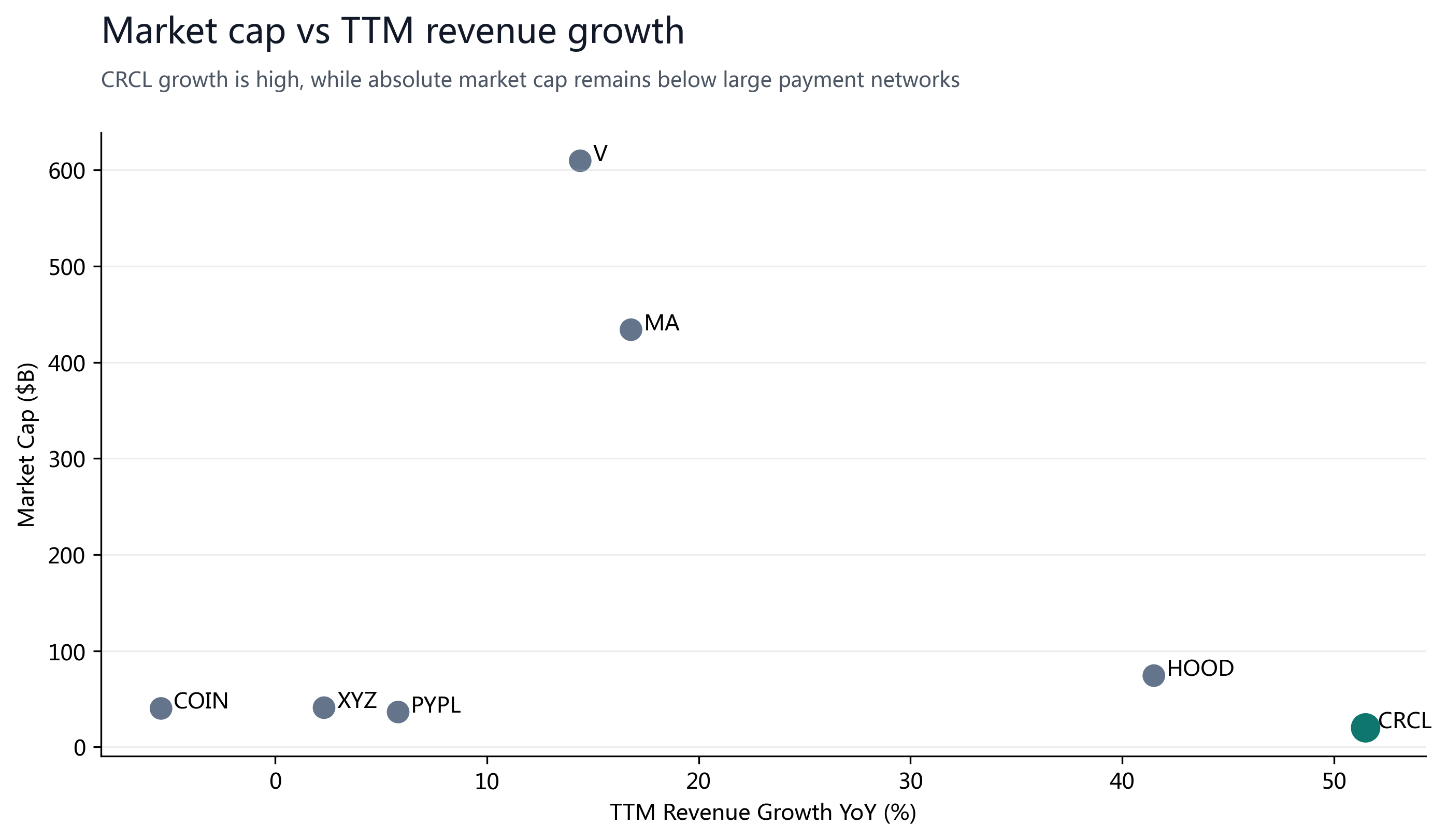

CRCL has no perfect peer: COIN is a crypto exchange, HOOD is a retail financial platform, PYPL/XYZ are payment fintechs, and V/MA are mature payment networks. We therefore do not blindly apply a peer median; we place CRCL in a valuation band between crypto infrastructure and payment networks.

| Ticker | MCap | TTM Rev Growth | P/S | Fwd PE |

|---|---|---|---|---|

| CRCL | $19.96B | +51.5% | 7.0x | 65.45x |

| COIN | $40.15B | -5.4% | 6.4x | 58.07x |

| HOOD | $74.26B | +41.5% | 16.1x | 41.46x |

| PYPL | $36.42B | +5.8% | 1.1x | 7.62x |

| XYZ | $40.94B | +2.3% | 1.7x | 16.35x |

| MA | $433.91B | +16.8% | 12.8x | 24.26x |

| V | $609.57B | +14.4% | 14.2x | 23.22x |

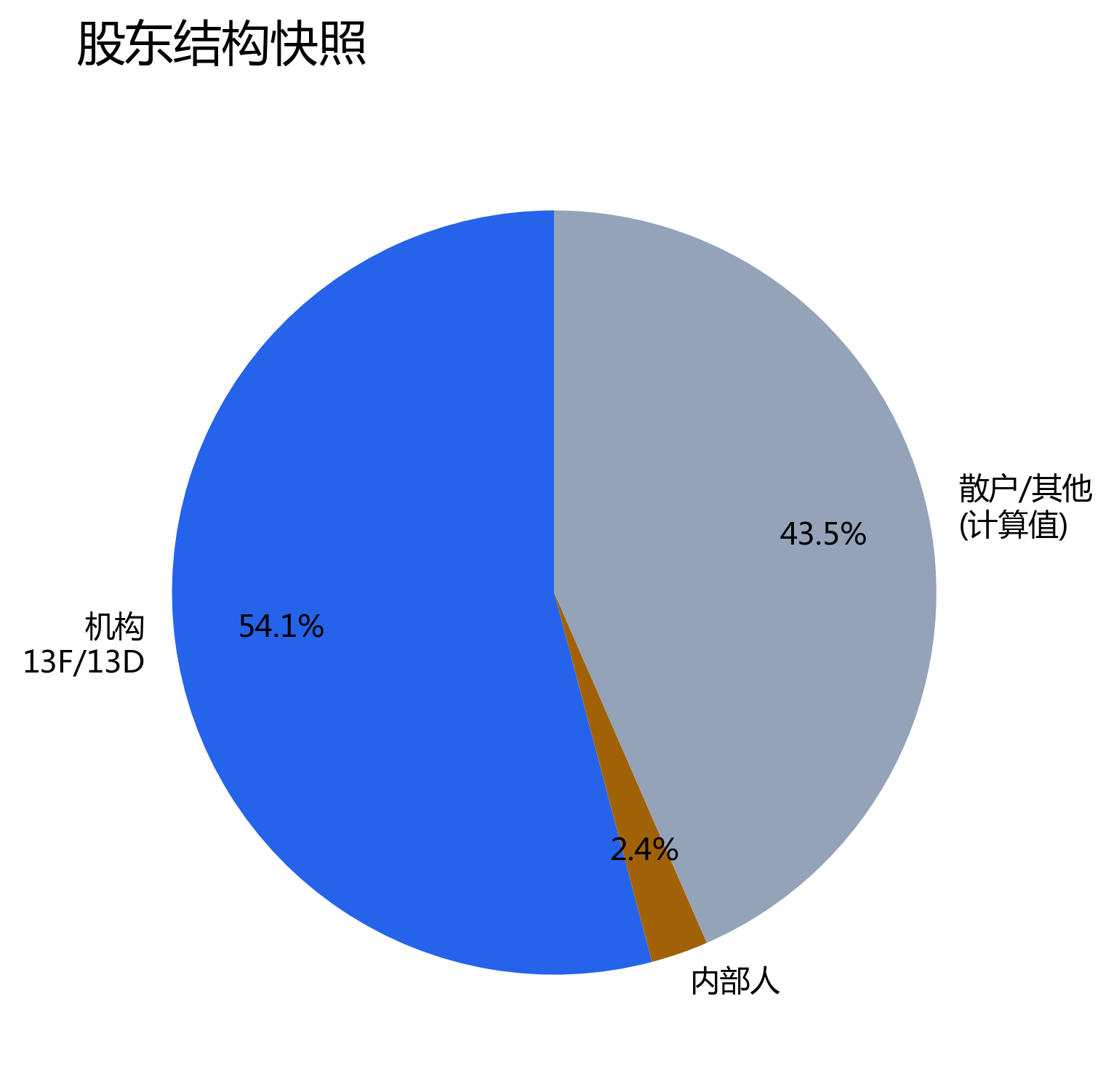

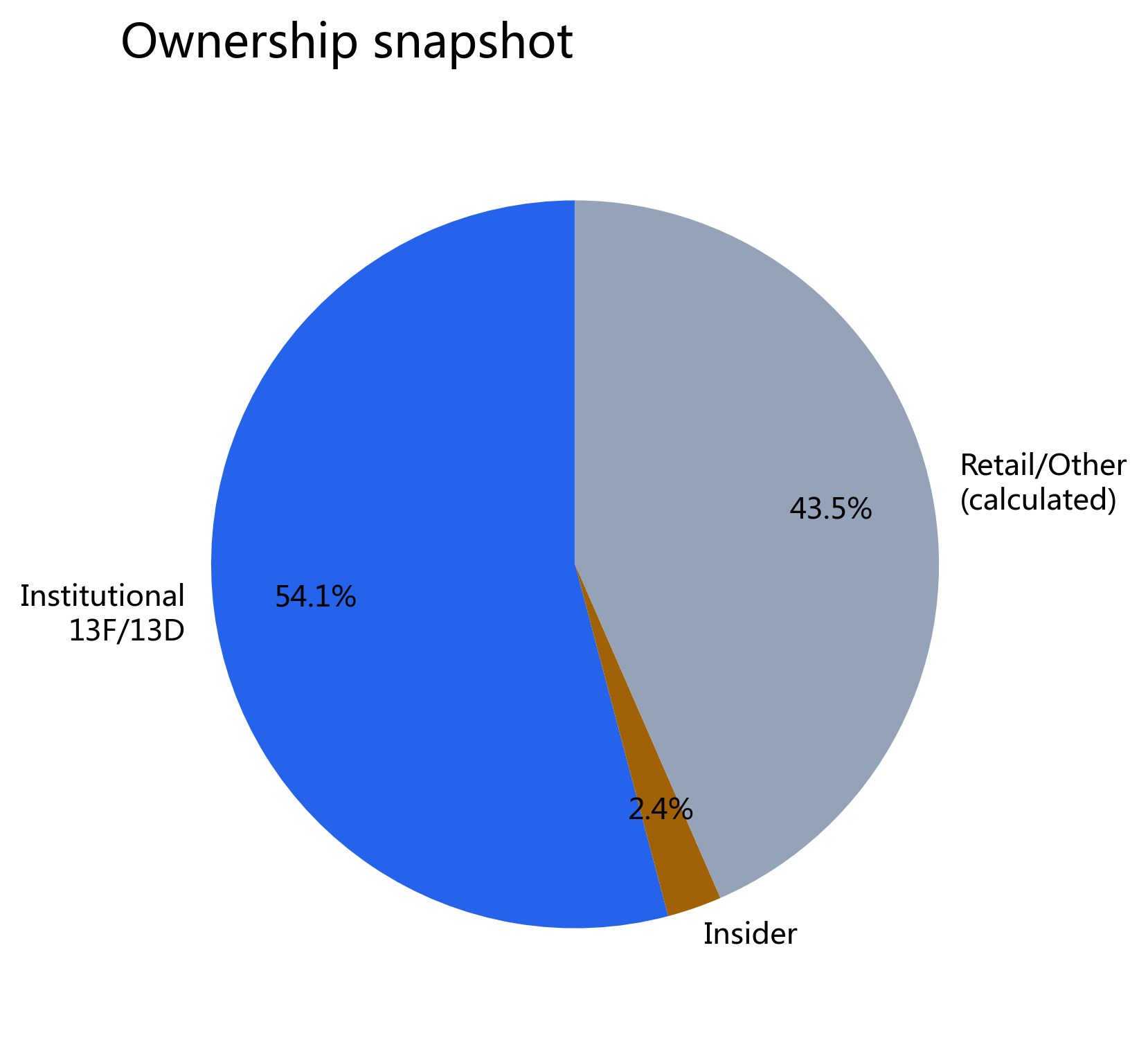

§06Ownership

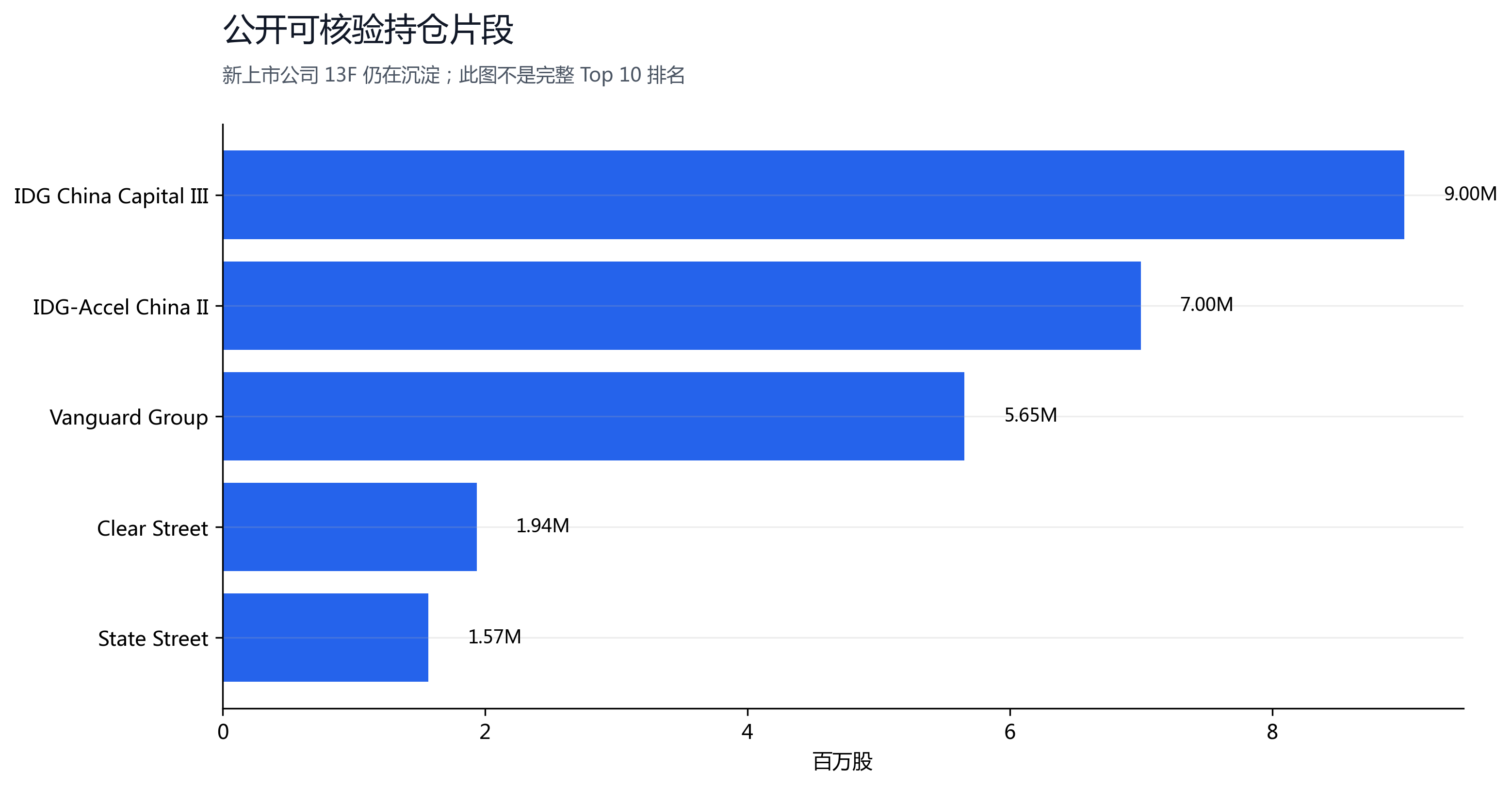

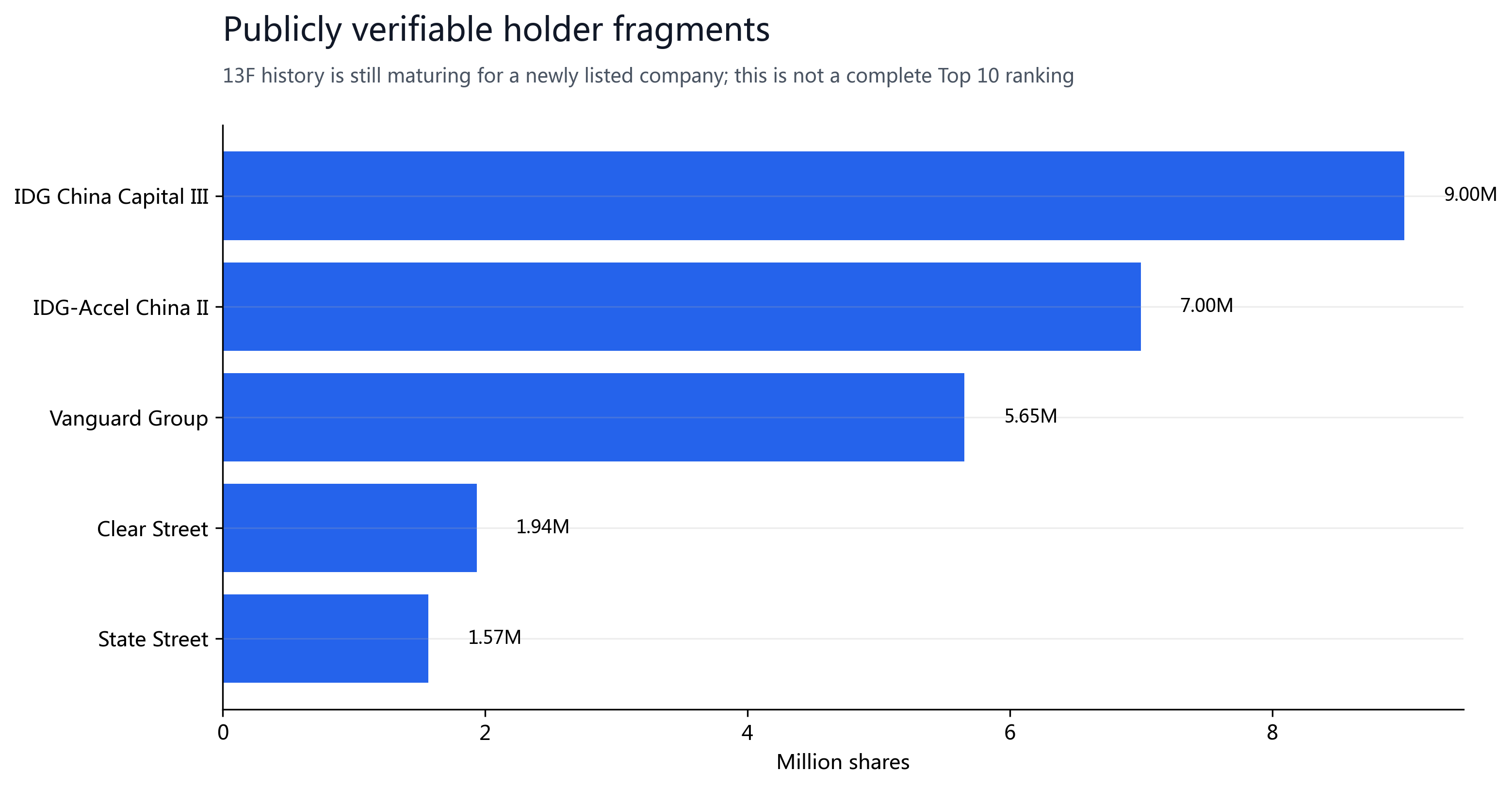

Fintel is a data site tracking institutional ownership and 13F/13D filings. Its CRCL page shows 555 institutional/13F/13D holders, with institutional long shares of about 124.4M, or about 54.12%. Because CRCL listed in 2025, 13F data is still maturing; any 'Top 10' chart must be labeled as publicly verifiable fragments rather than a complete ranking.

§07Valuation and Price Target

| Method | Formula | PT | Weight |

|---|---|---|---|

| Revenue multiple | FY26E $3.0B × 9.0x / 248.58M | $109 | 35% |

| RLDC multiple | (FY26E $1.25B × 23x + $1.52B cash) / 248.58M | $122 | 30% |

| Adj EBITDA multiple | (FY26E $0.65B × 43x + $1.52B cash) / 248.58M | $119 | 20% |

| Street PT check | Consensus avg $143.48, haircut to $135 | $135 | 15% |

| Weighted PT | 0.35×109 + 0.30×122 + 0.20×119 + 0.15×135 | $119 | 100% |

We round the weighted $119 result to $120. Note: CRCL's $76.78B deposits from stablecoin holders are pass-through redemption liabilities and must not be treated as normal corporate debt in an EV bridge; valuation uses only $1.517B corporate cash and $0 convertible debt after conversion.

§08Catalysts and Risks

| Date / Window | Event | Direction |

|---|---|---|

| 2026-06-16 to 2026-06-17 | FOMC + SEP | Rate path affects reserve income and valuation multiples |

| 2026-07 to 2026-09 | Stablecoin regulatory implementation / platform competition headlines | Regulatory clarity helps; Visa/Mastercard/Stripe competition hurts |

| 2026-08 | Q2'26 earnings | Validate USDC circulation, RLDC margin, and adjusted EBITDA |

§09Sources, Limits and Disclosure

- Circle Q1'26 results: https://www.circle.com/pressroom/circle-reports-first-quarter-2026-results

- Circle FY2025 10-K and Q1'26 10-Q: https://www.sec.gov/Archives/edgar/data/1876042/

- Market data and analyst consensus: https://stockanalysis.com/stocks/crcl/ and /forecast/

- Stablecoin market data: https://coinmarketcap.com/view/stablecoin/ (live page; build-time snapshot captured on 2026-06-08)

- Rates: Federal Reserve H.15 release, June 5, 2026

- Institutional ownership: Fintel CRCL institutional ownership public page; snapshot captured on 2026-06-08; partial holder values are public fragments, not a complete ranking

Limitations: CRCL is newly listed, so public trading history and 13F history are short; ch10 is not a complete institutional Top 10; 2026E-2028E are author estimates; this report is not investment advice.